So you’re thinking about getting your very own BTO flat in Singapore? That’s a huge milestone—and let’s be honest, the process can feel a bit overwhelming at first. But hey, you’re not alone! I’ve got your back with this step-by-step guide that will walk you through how to apply for a BTO flat in Singapore, no jargon, no fuss.

From checking if you qualify to gathering the right documents, applying for your HFE letter, and finally submitting that all-important BTO application, I’ll break down every step in a way that’s super easy to follow.

Whether you’re a first-timer or just need a refresher on the process in 2025, you’ll find everything you need to kickstart your BTO journey right here.

Ready to get started? Let’s dive in and make your homeownership dreams a reality!

Step 1: Check Your Eligibility

Before you even think about applying for a BTO flat, it’s crucial to know if you meet the eligibility requirements set by HDB. Trust me, getting this step right saves you time (and headaches) later on. Here’s how to get started:

Ensure You Meet Citizenship and Age Criteria

To apply for a BTO flat in Singapore, you (and your co-applicant, if any) need to tick a few essential boxes:

Citizenship:

- At least one applicant must be a Singapore Citizen (SC).

- For couples, the other applicant can be either an SC or a Singapore Permanent Resident (SPR).

Age:

- You must be at least 21 years old to apply.

My tip for you is if you’re applying under the Fiancé/Fiancée Scheme, you’ll need to register your marriage within three months of collecting your keys.

Understand Income Ceilings and Private Property Rules

Your household income—and whether you currently own any property—can make or break your BTO application. Here’s what you need to know:

Income Ceiling Guidelines for BTO Applicants (2025)

| Flat Type | Income Ceiling (Monthly) |

|---|---|

| 2-room Flexi | Up to $7,000 |

| 3-room | Up to $7,000 or $14,000 |

| 4-room and above | Up to $14,000 |

| Multi-Gen | Up to $21,000 |

Private Property Ownership:

- You (or any listed applicant) must not own or have disposed of any private property (in Singapore or overseas) in the last 30 months before your application.

It’s always wise to double-check these income limits before applying, especially if you’ve had recent job changes. You wouldn’t want to miss out on that dream home because of a technicality.

Form the Right Family Nucleus for Application Success

HDB requires applicants to form what they call a family nucleus. Sounds official, but it’s simpler than it sounds:

Who Qualifies as a Family Nucleus?

- Married couples (including those applying under the Fiancé/Fiancée Scheme)

- Parents applying with children

- Single applicants aged 35 and above (only eligible for 2-room Flexi flats in non-mature estates)

Singles, take note: Applying under the Joint Singles Scheme with up to three other singles is also an option, but your choices are limited to 2-room Flexi flats.

Step 2: Prepare Your Documents

Now that you’ve confirmed your eligibility, let’s talk about gathering the right documents for your BTO application. Trust me, having everything ready saves you stress and speeds up the process. Here’s what you’ll need:

Gather NRICs and Essential Identification

First things first—HDB needs to know who’s applying. Make sure you have these identification documents on hand:

- NRICs for all applicants (including co-applicants)

- Birth certificates for children or other dependents (if applicable)

- Marriage certificate (if you’re applying as a couple)

Make sure your personal details, especially your NRIC number, are accurate before submitting your application.

Compile Income Proof to Support Your Application

HDB uses your income documents to determine your eligibility and assess grants or loan options. Here’s what to prepare:

- Latest 12 months’ payslips or CPF contribution statements

- Income tax statements if you’re self-employed or have variable income

- Bonus or variable pay documentation (if applicable)

Why it matters:

Your income proof is essential not just for eligibility, but also for assessing your eligibility for housing grants like the Enhanced CPF Housing Grant (EHG).

For an easy way to estimate your potential monthly payments, try Ace Mortgage’s home loan repayment calculator. You can also explore Singapore home loan rates to compare what’s best for your situation.

Include Documents for Special Schemes Like Fiancé/Fiancée Applications

Applying under the Fiancé/Fiancée Scheme or other special schemes? Make sure you’ve got:

- Proof of engagement (for Fiancé/Fiancée applicants)

- Statutory Declaration of Intent to Marry (if you’re applying as an engaged couple)

- Court documents (if applicable) for applicants who are divorcees or widowed

Personal Insight:

These documents can be easy to overlook, especially for first-timers. Having them ready early can help you avoid any last-minute scrambling.

For more on special eligibility schemes, visit Ace Mortgage’s BTO eligibility guide and learn about different options available for couples, singles, and families.

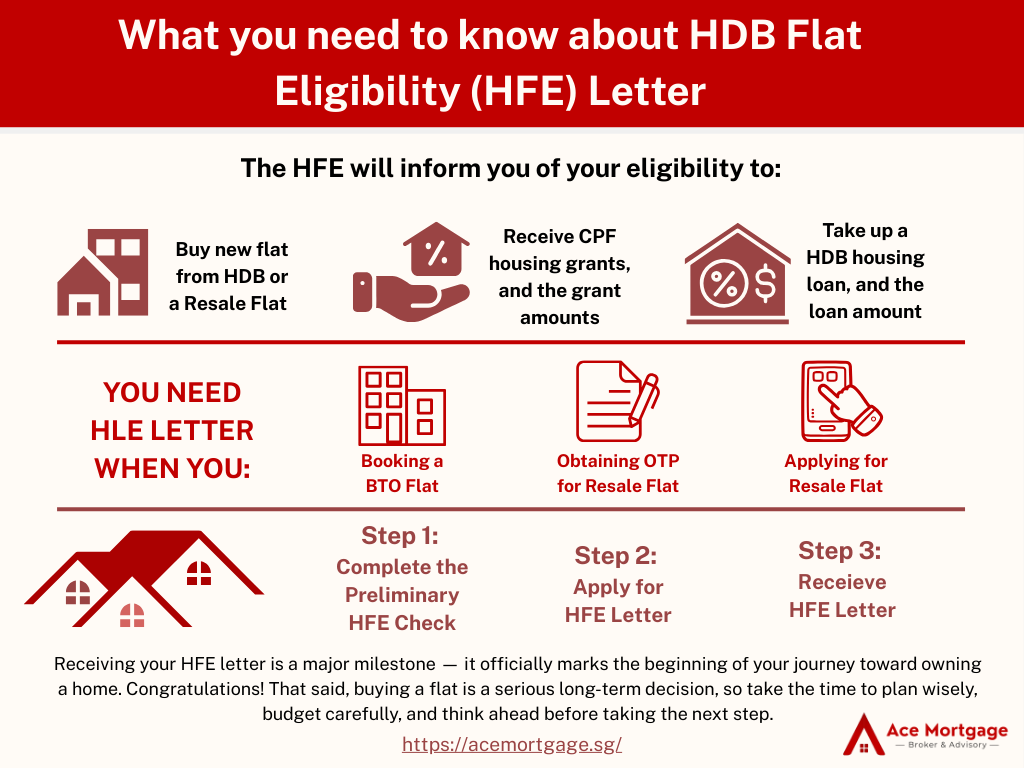

Step 3: Apply for the HDB Flat Eligibility (HFE) Letter

Once you’ve got your documents in order, it’s time to tackle one of the most important steps in the BTO journey: applying for the HDB Flat Eligibility (HFE) Letter.

Think of this as your official ticket to apply for a BTO flat—without it, you won’t be able to proceed.

Why the HFE Letter is Key to the BTO Application

The HFE Letter does more than just confirm your eligibility—it also determines your housing grant eligibility and home loan options. Here’s why it matters:

- Confirms that you meet key criteria like citizenship, age, income, and family nucleus.

- Provides a clear picture of the grants you qualify for, such as the Enhanced CPF Housing Grant (EHG).

- Lets you know whether you’re eligible for an HDB loan, a bank loan, or both—crucial for financial planning.

Knowing whether you qualify for an HDB loan or need to consider a bank loan can impact your monthly payments.

Use Ace Mortgage’s mortgage calculator to estimate your payments and budget accordingly

Step-by-Step Guide to Applying for the HFE Letter Online

Applying for the HFE Letter is a straightforward process, but it’s important to get it right to avoid delays. Here’s how to do it:

- Log in to the HDB Flat Portal using your Singpass.

- Fill in your personal details, household information, and upload supporting documents.

- Review all information carefully before submitting your application.

What to Do If Your HFE Application is Delayed

While most HFE Letters are processed within 21 working days, delays can happen. Here’s what to do if yours takes longer:

- Check for incomplete documents — missing payslips or incorrect NRIC details are common culprits.

- Log in to the HDB Flat Portal to track your application status.

- Contact HDB if you need assistance or clarification on your application.

If you’re worried about financing while you wait, reach out to a trusted mortgage advisor at Ace Mortgage who can guide you through your loan options and help you stay on track.

Step 4: Monitor Upcoming BTO Launches

Once you’ve got your HFE Letter approved, it’s time to start planning which BTO project to apply for. Staying updated on upcoming BTO launches is key to choosing the best home for your needs—and boosting your chances in the ballot.

Use HDB eAlerts to Stay Ahead of Launch Dates

Nobody wants to miss out on a great launch date! Sign up for HDB’s eAlerts service to receive notifications straight to your inbox.

Why eAlerts matter:

- Get notified of new launches as soon as they’re announced.

- Stay informed about project locations and application windows.

Expert Tip:

Bookmark Ace Mortgage’s homepage for the latest mortgage rates and expert home loan advice—this can help you plan your finances even before the launch.

For official launch schedules and upcoming projects, head over to HDB’s BTO Launch page.

Compare Projects for the Best Fit for Your Needs

Every BTO project is different. Compare key factors like location, amenities, and connectivity before making a decision.

What to consider:

- Proximity to MRT stations, schools, and shopping centers.

- Estate maturity (mature vs. non-mature).

- Future developments in the area.

Use Ace Mortgage’s home loan calculator to estimate monthly payments based on your budget and preferred project. For more project comparison tips, check out Ace Mortgage’s guide to home loan rates.

Decide Whether to Opt for the Optional Component Scheme (OCS)

The OCS lets you add finishes like flooring, doors, and sanitary fittings to your flat. This can save time and effort—but is it worth it?

Pros of OCS:

- Move-in ready unit with basic finishes done.

- Potential cost savings compared to hiring contractors later.

Cons of OCS:

- Less flexibility for customization.

- Finishes may not match your personal taste.

If you’re looking for convenience, OCS is great. But if you have a unique style in mind, you might want to skip it.

Step 5: Submit Your BTO Application

Ready to turn your housing dreams into reality? Once you’ve chosen your preferred project, it’s time to submit your BTO application through the HDB Flat Portal. This is your official chance to secure a unit—so let’s make sure you do it right!

Navigate the HDB Flat Portal Like a Pro

Applying online is quick and convenient, but it’s easy to get overwhelmed. Here’s how to breeze through the HDB Flat Portal:

- Log in using your Singpass account.

- Select the BTO project you’re interested in.

- Choose your preferred flat type and location.

- Review all your details before clicking “Submit.”

Need help with mortgage planning? Check out Ace Mortgage’s guide to Singapore home loan rates for expert advice on financing your dream home.

Make Smart Flat and Location Choices

Before hitting submit, think carefully about the unit type and location that best suits your lifestyle and budget:

- Flat Type: Consider your household size and future needs—2-room Flexi, 3-room, 4-room, or 5-room?

- Location: Proximity to MRT stations, schools, and amenities can boost your long-term investment value.

- Budget: Use Ace Mortgage’s home loan calculator to estimate your monthly payments and ensure affordability.

Expert Tip:

Don’t just pick the most popular project—look for units that align with your lifestyle and future plans.

Avoid Mistakes When Paying the Application Fee

Paying the application fee might seem straightforward, but a few common mistakes can cause delays:

- Check the correct fee: $10 for 2-room Flexi flats, $20 for other flat types.

- Use approved payment methods: eNETS, AXS, or other options listed on the HDB Flat Portal.

- Double-check payment confirmation: Save your receipt or screenshot as proof.

Step 6: Improve Your Chances in the BTO Ballot

Winning a BTO flat can feel like hitting the jackpot, but it’s not all luck—there are ways to increase your chances. Here’s how you can stack the odds in your favor and secure the flat of your dreams:

Apply Under Priority Schemes to Gain an Edge

Priority schemes are HDB’s way of giving certain groups—like parents with young kids or those living near family—an extra boost in the ballot. Here’s what’s available:

- Parenthood Priority Scheme (PPS): For married couples with at least one child.

- Married Child Priority Scheme (MCPS): If you’re buying a flat near your parents or vice versa.

- Multi-Generation Priority Scheme (MGPS): For parents and married children applying together.

Expert Tip:

Always apply under every scheme you qualify for—it’s free and can seriously improve your ballot chances. For more details on these schemes, visit HDB’s Priority Schemes guide.

Consider Less Popular Estates for Higher Success Rates

Non-mature estates often have more flats available and fewer applicants, meaning your chances of success are higher.

Benefits of Non-Mature Estates:

- Higher supply of units.

- More affordable prices.

- Potential for future growth and amenities.

Thinking about your financing? Check out Ace Mortgage’s home loan calculator to see how your monthly payments stack up, especially if you’re considering different estates and unit sizes.

Use First-Timer Benefits to Your Advantage

First-timer applicants get extra priority during the BTO ballot—take advantage of it!

What You Get as a First-Timer:

- More chances in the ballot compared to second-timer applicants.

- Higher allocation in both mature and non-mature estates.

- Access to grants like the Enhanced CPF Housing Grant (EHG).

Use this advantage wisely—pair it with a less popular estate or a priority scheme to maximize your chances of success.

Step 7: What Happens After Submitting Your Application?

Congrats—you’ve officially submitted your BTO application! But what happens next? Let’s walk you through what to expect after you hit that “submit” button.

How to Interpret Your Ballot Results

HDB uses a computerised ballot system to allocate flats—so how do you read your results?

- Ballot Number: A lower number means an earlier chance to pick your flat, while a higher number might put you on the waitlist.

- Available Units: Compare your ballot number to the total number of flats offered in your chosen project.

- Waitlist: Even if your number is higher than the total flats, don’t give up—sometimes people drop out, giving you a shot.

For a quick budgeting check, use Ace Mortgage’s mortgage loan calculator to plan your monthly payments once you secure a unit.

Prepare for Booking Your Flat and Signing the Lease

If you get invited to book a flat, here’s what you need to know:

- Booking Appointment: You’ll select your preferred unit and pay the option fee ($500–$2,000 depending on flat type).

- Required Documents: Bring NRICs, HFE Letter, marriage certificate (if applicable), and income documents.

- Signing the Lease: This is when you make your down payment (via CPF or cash).

What to Check Before Collecting Keys and Moving In

Before you collect your keys and get ready to move in, here’s a handy checklist:

- Key Collection: HDB will notify you via SMS or letter with the appointment details.

- Payments: Complete the remaining down payment, stamp duty, and legal fees.

- Flat Inspection: Check for any defects—HDB provides a 1-year warranty for certain issues.

My personal opinion would be to bring along a checklist of what to inspect—walls, floors, fittings, and windows—so you can flag any defects right away.

For financial planning, visit Ace Mortgage’s homepage to explore budgeting and home loan rates before moving in.

Common Mistakes to Avoid When Applying for a BTO Flat

Applying for a BTO flat is a huge step, and it’s easy to slip up if you’re not careful. Let’s make sure you avoid the most common mistakes that can slow down your homeownership journey or cost you your dream flat.

Don’t Miss Key Deadlines or Application Windows

HDB’s application windows are usually open for about a week each quarter, and missing them can mean waiting months for the next launch.

- Set reminders for launch announcements and deadlines.

- Bookmark the HDB Flat Portal for quick access.

Subscribe to eAlerts from HDB so you never miss a launch.

Double-Check All Documents to Avoid Rejections

Submitting incomplete or incorrect documents is one of the fastest ways to get your application rejected.

- Review all NRIC details and ensure they match your application.

- Check income documents for accuracy and completeness.

- Double-check special documents like statutory declarations for the Fiancé/Fiancée Scheme.

I always recommend creating a simple document checklist for yourself—it might sound basic, but it’s a real lifesaver when you’re rushing to submit your application and can’t remember if you’ve uploaded that payslip or marriage certificate!

Avoid Overextending Your Budget When Selecting a Flat

It’s tempting to go for the biggest, fanciest unit—but make sure you can truly afford it.

- Calculate your monthly payments using Ace Mortgage’s mortgage loan calculator so you’re not overcommitted.

- Factor in renovation costs, furniture, and moving expenses.

- Leave a buffer for unexpected expenses or emergencies.

Final Thoughts: Your Complete Guide to Applying for a BTO Flat in Singapore

And there you have it—a complete, step-by-step guide on how to apply for a BTO flat in Singapore. By checking your eligibility, gathering the right documents, applying for the HFE Letter, and staying smart about your choices during the ballot, you’re setting yourself up for BTO success in 2025.

Remember, applying for a BTO flat doesn’t have to be stressful if you plan ahead and stay informed. Stay updated on upcoming BTO launches, keep your documents ready, and consider using expert mortgage advice to guide your financing decisions.

Ready to make your BTO dreams a reality?

Visit Ace Mortgage’s homepage for the latest mortgage rates, expert tips, and personalized advice on securing the best home loan in Singapore. Don’t forget to check out their mortgage loan calculator to budget confidently before you apply. Here’s to your future home—good luck!