Thinking of buying a house in Singapore? It’s an exciting milestone—but it also comes with a long list of costs and fees that can quickly add up. From stamp duties and legal fees to valuation charges and agent commissions, knowing what to expect can help you budget wisely and avoid surprises.

In this guide, we’ll break down the full list of costs—including hidden ones—so you can make smarter financial decisions. We’ll also cover the latest on home loan rates in Singapore (with insights from Ace Mortgage), plus tips on finding the best deals. Whether you’re buying an HDB flat or a private condo, this article has you covered.

Let’s dive in.

Complete Breakdown of Upfront Costs for Buying a House in Singapore

Understanding the upfront costs of buying a house in Singapore is crucial to avoid surprises. These costs go beyond the property price—covering everything from application fees to down payments and legal charges. Whether you’re eyeing an HDB flat or a private property, knowing what to expect helps you budget wisely and secure the best home loan rates in Singapore.

Below, we break down each component so you can plan confidently for your home purchase.

Application and Administrative Fees — What to Expect

Application and administrative fees may seem minor, but they add up quickly. Here’s what you’ll need to pay:

- HDB Application Fee:

- Typically $10 for 2-room Flexi flats, $20 for 3-room and above (HDB Official Guide).

- Typically $10 for 2-room Flexi flats, $20 for 3-room and above (HDB Official Guide).

- Resale Application Admin Fee:

- Around $40–$80, depending on the flat size.

- Covers processing and eligibility checks.

- Around $40–$80, depending on the flat size.

💡 Expert Tip: Always keep receipts for these fees, as they might come in handy when tracking overall home-buying costs.

For private properties, administrative fees vary by developer and project—so always clarify with the sales team before signing any documents.

Related Link: Singapore Home Loan Rates — compare the latest rates before you commit.

Option to Purchase (OTP) and Exercise Fees

Once you select your dream home, you’ll need to pay an Option to Purchase (OTP) fee to secure it. Here’s how it works:

OTP & Exercise Fee Comparison: HDB vs Private Property

| Fee Type | HDB Flats | Private Property |

|---|---|---|

| OTP Fee | $1–$2,000 (HDB Guide) | Typically 1% of purchase price |

| Exercise Fee | Up to 20% of purchase price (less OTP paid) | Usually 4% of purchase price |

- For HDB Flats:

- Pay the OTP fee when you get the Option.

- Exercise fee (minus OTP) is due within 21 days.

- Pay the OTP fee when you get the Option.

- For Private Properties:

- OTP fee secures the unit.

- Exercise fee brings the total to 5% of the purchase price.

- OTP fee secures the unit.

Expert Tip: Budget for these payments using both cash and CPF. Confirm with your mortgage broker Singapore to see how this aligns with your financing plan.

Minimum Down Payment Requirements (Cash, CPF, Grants)

Your down payment is often the biggest upfront cost. Here’s what you need to know:

- For HDB Flats with HDB Loan:

- Minimum 20% down payment (fully payable via CPF).

- Minimum 20% down payment (fully payable via CPF).

- For HDB Flats with Bank Loan:

- Minimum 25% down payment:

- 5% cash (must be paid upfront)

- 20% CPF or cash

- 5% cash (must be paid upfront)

- Minimum 25% down payment:

- For Private Property:

- Minimum 25% down payment:

- 5% cash

- 20% CPF or cash

- 5% cash

- Minimum 25% down payment:

HDB vs Bank Loan Cash & CPF Requirements

| Loan Type | Cash Requirement | CPF / Cash Portion | Notes |

|---|---|---|---|

| HDB Loan | 0% (CPF OK) | 20% CPF | HDB loan interest rate is typically stable |

| Bank Loan | 5% | 20% | Rates vary, so compare carefully |

Expert Tip: Check the latest mortgage interest rates in Singapore using Ace Mortgage’s home loan repayment calculator to determine monthly affordability. Also, tap into CPF housing grants if you’re eligible—they can significantly reduce your cash outlay.

Legal and Conveyancing Fees in Singapore

Legal fees are a crucial part of the homebuying process in Singapore, covering the conveyancing work that ensures your property transaction is smooth and legally secure.

Whether you’re buying an HDB flat or a private property, understanding these fees helps you plan your budget and avoid surprises.

Why You Need a Conveyancing Lawyer

A conveyancing lawyer handles the paperwork, conducts due diligence, and protects your interests in a property transaction. Here’s why they’re essential:

- Title Checks: Ensures the property’s title is clear and free from encumbrances.

- Document Preparation: Prepares the Sale & Purchase Agreement and liaises with the HDB or private seller.

- Funds Handling: Manages payments, including the Option to Purchase (OTP) and stamp duties.

Expert Tip: Always engage a conveyancing lawyer familiar with both HDB and bank loans—this helps you navigate issues like refinancing and ensures smooth coordination with your mortgage loan Singapore application. For a list of licensed conveyancers, check the Law Society of Singapore.

Typical Legal Fees for HDB and Private Properties

Legal fees vary based on the property type, complexity of the transaction, and the lender you choose. Here’s a general guide:

Typical Legal Fees for HDB Flats and Private Properties

| Property Type | Typical Legal Fees (2025) | Notes |

|---|---|---|

| HDB Flat | $2,000 – $2,500 (inclusive of GST) | Often includes mortgage stamping fees. |

| Private Condo | $2,500 – $3,500 (inclusive of GST) | May vary based on complexity and loan amount. |

Expert Tip: Some banks or mortgage brokers, like Ace Mortgage, may offer discounted legal fees as part of their home loan packages—so be sure to ask before committing.

For official guidance on legal fees, visit HDB’s legal fees overview.

Additional Legal Costs — Caveats, Title Searches, Document Fees

Beyond the standard legal fees, watch out for extra costs that often get overlooked:

- Caveat Lodgement: Typically $150–$200 — this protects your interest in the property during the transaction.

- Title Search Fees: Around $100 — essential for verifying the seller’s legal right to sell.

- Miscellaneous Document Fees: $100–$300 — covers CPF charge registration and other required paperwork.

Breakdown of Additional Legal Costs in Singapore

| Legal Item | Typical Cost (2025 | Notes |

|---|---|---|

| Caveat Lodgement | $150–$200 | Required to secure your claim |

| Title Search Fees | $100 | Confirms no encumbrances |

| Document Fees | $100–$300 | CPF charges and related documents |

Expert Tip: Ask your conveyancing lawyer for a complete, itemized breakdown of all legal fees upfront—this helps you budget effectively and prevents unexpected charges later on.

And don’t forget—keeping an eye on current home loan rates can help you make smarter decisions about when and how to buy your dream home.

Singapore Stamp Duties — BSD and ABSD Explained

Stamp duties are among the largest upfront costs when buying a house in Singapore—and they’re unavoidable. Whether you’re a first-time buyer or an investor, understanding both Buyer’s Stamp Duty (BSD) and Additional Buyer’s Stamp Duty (ABSD) is essential to budget accurately and avoid financial surprises.

Let’s dive into what these taxes mean, how much you might pay, and how to estimate them effectively using reliable tools like the BSD calculator.

Buyer’s Stamp Duty (BSD) — Rates and Calculations

BSD applies to all property purchases in Singapore, whether it’s an HDB flat or a private condo. The rates are progressive and based on the property’s purchase price or market value (whichever is higher). Here’s the latest breakdown:

Buyer’s Stamp Duty (BSD) Rates in Singapore

| Property Value Bracket | BSD Rate (Residential) |

|---|---|

| First $180,000 | 1% |

| Next $180,000 | 2% |

| Next $640,000 | 3% |

| Amount exceeding $1 million | 4% |

For example, a $1.5 million condo purchase would result in:

- 1% on first $180,000 = $1,800

- 2% on next $180,000 = $3,600

- 3% on next $640,000 = $19,200

- 4% on the remaining $500,000 = $20,000

- Total BSD: $44,600

BSD can be paid using CPF savings (subject to CPF Board’s guidelines), which helps reduce cash outlay upfront. For a detailed breakdown and the latest updates, check the IRAS official site.

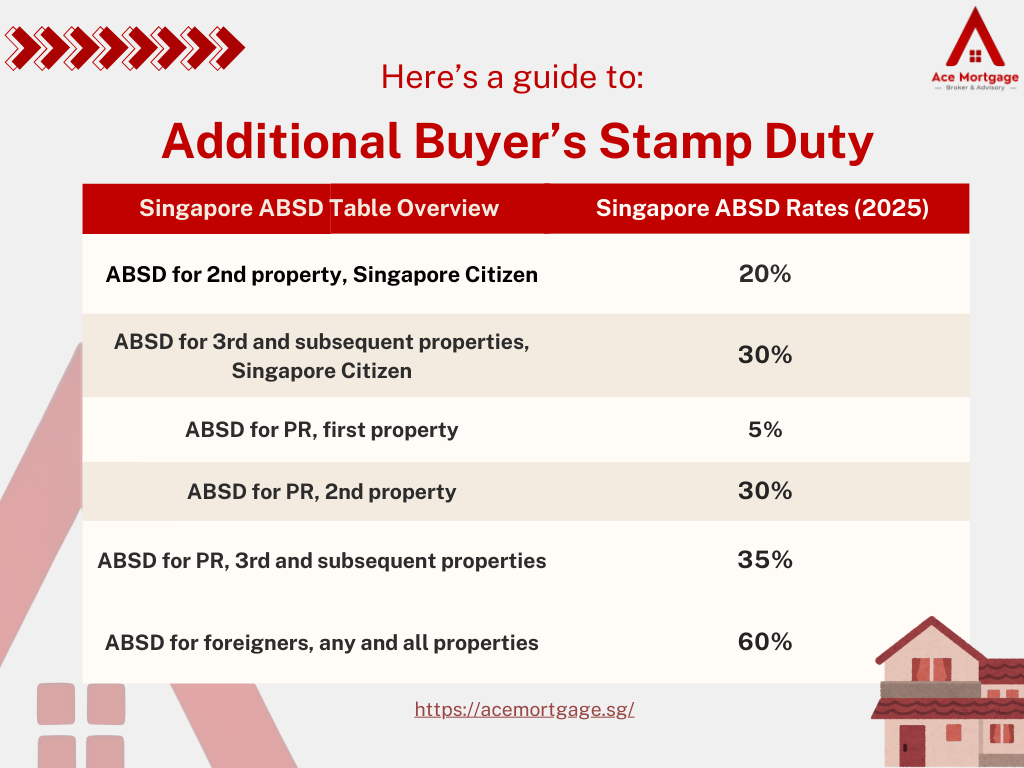

Additional Buyer’s Stamp Duty (ABSD) — Who Pays and How Much?

ABSD is an extra tax imposed on certain property buyers, depending on their residency status and the number of properties they own. Here’s who pays ABSD:

- Singapore Citizens:

- First property: 0%

- Second property: 20%

- Third and subsequent properties: 30%

- First property: 0%

- Singapore Permanent Residents (PRs):

- First property: 5%

- Second property: 30%

- Third and subsequent properties: 35%

- First property: 5%

- Foreigners and Entities:

- All properties: 60%

- All properties: 60%

Expert Tip: ABSD cannot be paid using CPF savings—it must be paid in cash. Always consider ABSD when evaluating your investment property strategy, and check with a mortgage broker in Singapore to plan your financing wisely.

For full details, refer to IRAS’s ABSD page.

Using a Stamp Duty Calculator — Plan Your Budget

Calculating BSD and ABSD manually can be time-consuming and prone to errors. That’s where a stamp duty calculator comes in handy. Tools like Ace Mortgage’s BSD Calculator allow you to:

- Input your property value and residency status

- Instantly view your BSD and ABSD obligations

- Plan your cash flow and CPF usage accordingly

Benefits of Using a Stamp Duty Calculator

| Benefits | Description |

|---|---|

| Fast and Accurate | No need for manual calculations or guesswork |

| Customised to Buyer Type | Adjusts automatically for residency status and property count |

| Budget-Friendly Planning | Helps align CPF and cash usage with purchase costs |

Always double-check calculator results with your conveyancing lawyer to ensure accuracy. And remember, BSD and ABSD are payable within 14 days of signing the Sale & Purchase Agreement—so plan your cash flow carefully.

Financing a House in Singapore — Loans, Interest Rates, and CPF

Getting the right financing is crucial when buying a home in Singapore. From loan-to-value (LTV) limits to interest rates and using your CPF savings, understanding how it all works helps you make the best decision for your budget and lifestyle. Let’s explore the key factors to watch.

Loan-to-Value (LTV) Ratios and Borrowing Limits

LTV limits determine how much of your property’s value you can borrow.

- First housing loan: Up to 75% LTV if the loan tenure is ≤ 30 years and you’re under 65.

- Second housing loan: Up to 45% LTV.

- Third and subsequent loans: Up to 35% LTV.

LTV Ratios for Residential Properties

| Loan Count | Maximum LTV Ratio |

|---|---|

| First Loan | Up to 75% |

| Second Loan | Up to 45% |

| Third or More | Up to 35% |

Tip: Always check your eligibility with your bank or a mortgage broker in Singapore to avoid surprises. For an updated list of rates and restrictions, visit the Monetary Authority of Singapore.

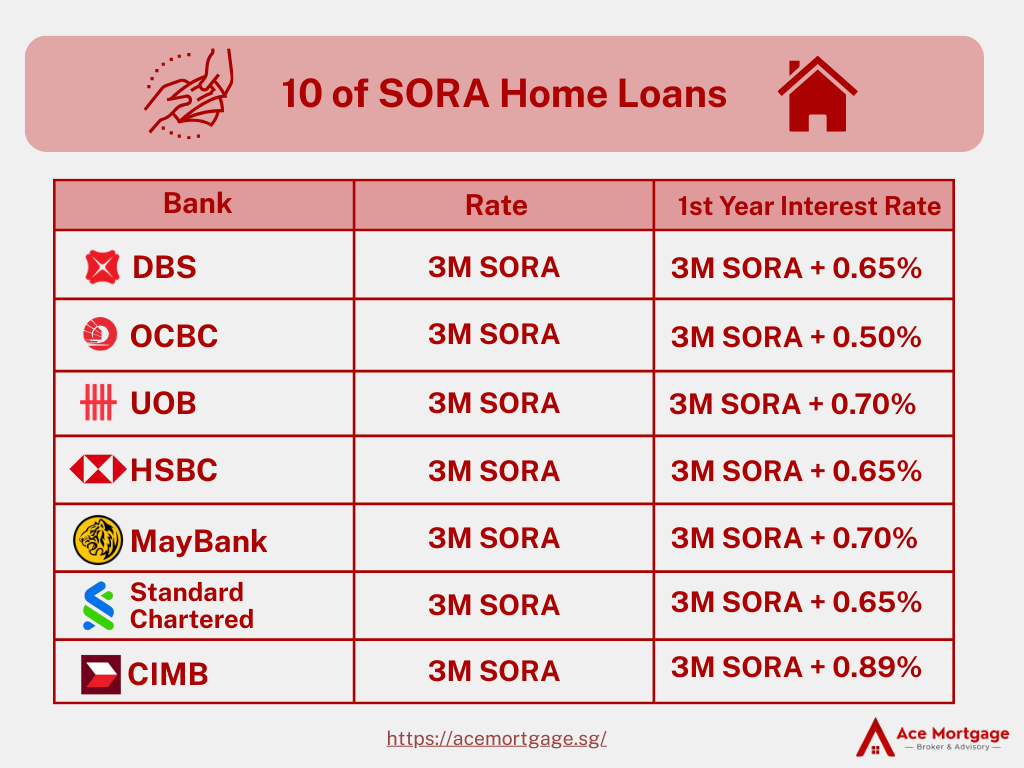

Home Loan Interest Rates in Singapore — What’s Trending?

Interest rates in Singapore can vary widely. SORA-based loans continue to do well in the market, offering competitive rates. Fixed rates remain popular for buyers seeking stability.

- SORA packages: Often lower than fixed rates but can fluctuate.

- Fixed rates: Generally 1.5% to 1.8% as of early-2026, depending on the bank.

Tip: Compare rates across multiple banks with Ace Mortgage to find the best home loan rates Singapore-wide.

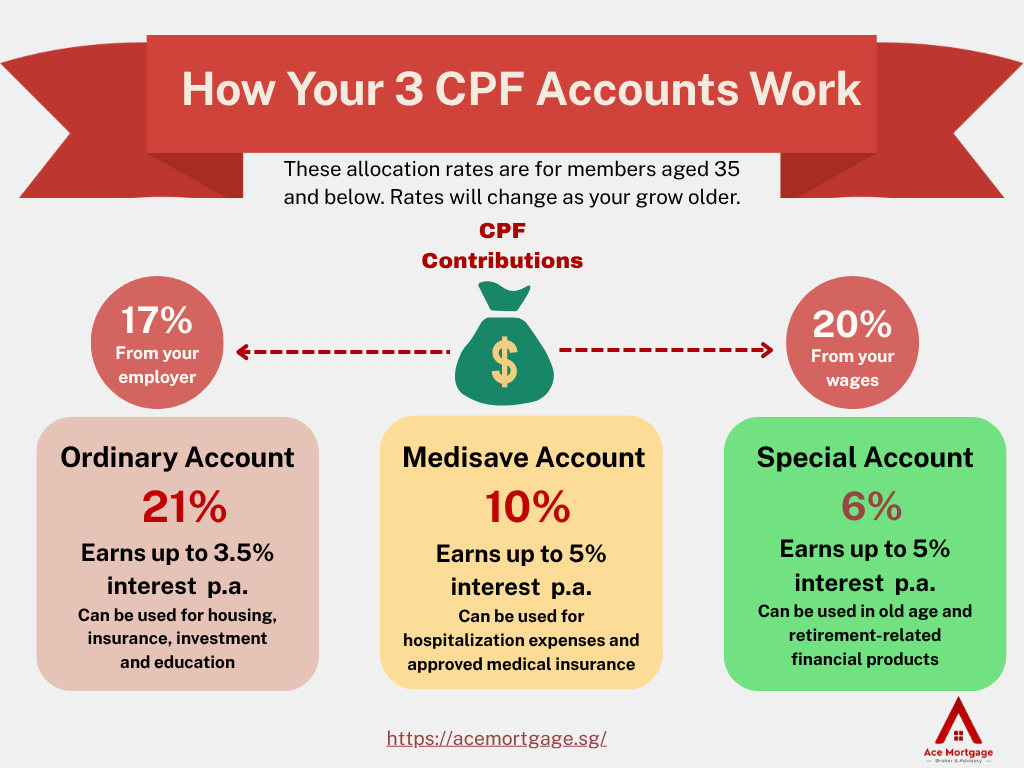

Using CPF for Down Payment and Monthly Installments

Your CPF Ordinary Account can fund part of your home purchase. Here’s how:

- Down Payment: Use CPF to cover the 20% (HDB loan) or up to 20% (bank loan) portion.

- Monthly Installments: CPF can also pay your monthly mortgage, reducing cash outlay.

Always plan your CPF usage wisely—depleting too much could impact future retirement savings. For detailed budgeting, use Ace Mortgage’s home loan repayment calculator to plan your monthly commitments.

Property Valuation and Its Impact on Financing

Before getting a home loan, banks and financial institutions require a property valuation to assess its market value. This valuation plays a big role in determining your loan amount and stamp duties—so it’s essential to understand how it works and what costs to expect.

How Property Valuation Works in Singapore

Property valuation in Singapore is typically conducted by a bank-appointed valuer. Here’s how it works:

- The valuer inspects the property, considering factors like location, size, condition, and recent transaction prices.

- A valuation report is then issued, stating the property’s estimated market value.

- Banks use this value to determine your loan-to-value (LTV) ratio, affecting how much you can borrow.

Tip: If you’re comparing home loans, check with your mortgage broker Singapore to understand how valuations influence financing limits.

For a deeper dive, the Council for Estate Agencies provides guidelines on property transactions and valuations.

Typical Costs for Property Valuation Reports

Valuation fees vary depending on the property type and value. Here’s what to expect:

Typical Property Valuation Fees

| Property Type | Estimated Cost (2025) |

|---|---|

| HDB Flats | $200 – $400 |

| Private Condos | $300 – $600 |

| Landed Properties | $500 – $800+ |

These fees are usually paid upfront when applying for a home loan. Some banks may absorb or rebate the fee as part of a loan package—so be sure to ask.

Tip: Always request an official receipt and keep it for tax or grant claims if applicable. You can also check Ace Mortgage to calculate your monthly payments based on your property’s value.

How Valuation Affects Loan Amount and Stamp Duties

A property’s valuation directly impacts how much you can borrow:

- Loan Amount: Banks apply the LTV ratio to the lower of the purchase price or valuation—so a lower valuation could mean you need a bigger cash down payment.

- Stamp Duties: BSD and ABSD are calculated based on the higher of the purchase price or market value.

To avoid surprises, confirm with your conveyancing lawyer and mortgage advisor how the valuation affects your financing and duties. For official guidance, refer to IRAS on BSD calculations.

Insurance and Taxes Every Homebuyer Should Know

Owning a home in Singapore means more than just paying your mortgage—there are ongoing costs like insurance and property taxes to consider. Knowing what’s mandatory and what’s optional helps you budget accurately and avoid costly surprises.

Mandatory Fire Insurance — HDB and Private Homes

Fire insurance is a must-have for all HDB flats with an outstanding housing loan. For private properties, banks usually require it as a loan condition.

- HDB Flats:

- Mandatory HDB Fire Insurance—basic coverage for structural damage.

- Premiums are affordable, often under $10 annually.

- Mandatory HDB Fire Insurance—basic coverage for structural damage.

- Private Homes:

- Required by banks as part of mortgage approval.

- Typically arranged through your lender.

- Required by banks as part of mortgage approval.

Tip: Always check your bank’s requirements. For better coverage, consider adding a home insurance policy. Compare different plans at Ace Mortgage before committing.

For details, visit the HDB Fire Insurance page.

Optional Home Insurance — Is It Worth It?

While fire insurance covers the structure, it doesn’t protect your renovations, contents, or personal belongings. That’s where optional home insurance comes in.

- Covers renovations, fixtures, and household contents.

- Often includes personal liability coverage.

- Annual premiums vary based on coverage and property size.

Even if it’s not mandatory, a comprehensive home insurance policy can save you thousands in unexpected repairs. Use Ace Mortgage’s Singapore mortgage advisors to explore suitable plans.

Annual Property Tax — How Much Will You Pay?

Every homeowner in Singapore must pay property tax annually, based on the Annual Value (AV) of the property.

- Owner-Occupied Residential Properties:

- Progressive rates starting from 0% to 16%.

- Progressive rates starting from 0% to 16%.

- Non-Owner-Occupied Properties (e.g., rental units):

- Higher rates apply, typically 12%–36%.

- Higher rates apply, typically 12%–36%.

Tip: The IRAS property tax calculator is your best friend when planning. For the latest rates and calculations, refer to the IRAS Property Tax page.

For a clearer picture of how taxes affect your financing, speak with a trusted mortgage advisor.

Renovation, Maintenance, and Upkeep Costs

Buying a house is just the beginning—renovation and ongoing maintenance costs can quickly add up. Whether it’s a brand-new BTO flat or a resale condo, knowing what to expect helps you avoid budget surprises and plan wisely.

Average Renovation Costs by Property Type

Renovation costs vary depending on the property type and extent of work. Here’s what homeowners can expect:

Average Renovation Costs in Singapore

| Property Type | Estimated Cost Range | Notes |

|---|---|---|

| HDB Flats | $20,000 – $60,000 | Basic works (painting, flooring) to full overhaul. |

| Condos | $40,000 – $80,000 | Includes built-ins and design upgrades. |

| Landed Homes | $100,000+ | Extensive customisation and higher finishes. |

Tip: Always get multiple quotes from contractors and check their credentials with the Building and Construction Authority (BCA) to avoid renovation pitfalls.

Factors That Influence Your Renovation Budget

Several factors can affect how much you spend on renovations:

- Scope of Work: A full overhaul costs more than basic touch-ups.

- Materials and Finishes: Premium finishes come at a premium price.

- Labor Costs: Vary depending on the contractor’s expertise and market demand.

- Design Complexity: Custom features and layouts require higher budgets.

Tip: Discuss with a mortgage broker Singapore if you plan to finance renovations with a renovation loan or as part of your housing loan.

Ongoing Maintenance, Conservancy, and Upkeep Costs

Once you move in, ongoing costs keep your home in good shape:

- Conservancy Fees (HDB): Typically $50–$90 per month, depending on flat type.

- Maintenance Fees (Condos): Usually $200–$500 per month, based on amenities.

- Repairs and Replacements: Annual budget of 1%–2% of property value recommended.

For a quick guide on managing these expenses, visit the HDB home maintenance page or talk to your mortgage advisor for tips on consolidating payments with your loan.

Hidden and Miscellaneous Costs When Buying a House

While upfront and legal fees are easy to plan for, hidden costs often catch buyers by surprise. From agent commissions to CPF opportunity costs, being aware of these expenses ensures you’re financially prepared and can make the best decision for your long-term budget.

Real Estate Agent Commissions — How Much and How to Negotiate

Agent commissions are one of the most common hidden costs when buying property in Singapore.

- Typical Rate: Usually 1%–2% of the purchase price, plus GST.

- Negotiation: Rates are negotiable; always clarify the commission rate before signing.

For new launches, developers often pay the agent’s fee—so you might not need to pay any commission. For resale properties, always factor this cost into your budget.

For more insights, the Council for Estate Agencies (CEA) provides guidelines on commission rates and practices.

Moving Expenses and Utility Setup — Often Overlooked Costs

It’s easy to focus on the big-ticket costs like stamp duties and legal fees, but moving expenses can add up quickly.

- Moving Costs: $500–$1,500 for standard moves (depending on distance and amount of furniture).

- Utility Setup: Deposits and activation fees for electricity, water, and internet typically range from $100–$300.

Remember to budget for renovations and furniture alongside these costs—use the Ace Mortgage home loan calculator to plan your finances wisely.

CPF Opportunity Costs — Is It the Best Use of Your Funds?

Using CPF savings to pay for your home is popular—but it comes with opportunity costs.

- Lost CPF Interest: Funds withdrawn from CPF no longer earn the guaranteed 2.5% annual interest.

- Accrued Interest Payback: If you sell the property, you must refund your CPF account the amount used plus accrued interest.

Always compare using CPF versus cash. In some cases, retaining CPF funds for retirement can be more beneficial in the long term.

Talk to your mortgage advisor to explore options that balance homeownership with retirement planning. For official CPF information, visit the CPF Board’s Housing Schemes page.

Final Thoughts on Buying a House in Singapore — Stay Informed and Plan Ahead

Buying a house in Singapore comes with many costs, from stamp duties and legal fees to renovation expenses and agent commissions. By understanding each cost upfront, you can budget wisely and avoid unpleasant surprises. Whether you’re a first-time buyer or upgrading to a new home, planning ahead is key to a smooth journey.

Ready to take the next step? Start by comparing the latest home loan rates in Singapore and explore your financing options with Ace Mortgage’s expert mortgage advisors. With the right guidance, you can navigate Singapore’s property market confidently and make the best decisions for your future.

Visit the Ace Mortgage homepage for more tools, tips, and the latest insights on buying a home in Singapore.