Trying to choose between the Deferred Payment Scheme (DPS) and Progressive Payment Scheme (PPS) for your new launch condo or EC? You’re not alone — this is one of the most common questions Singapore buyers ask.

Both options have big impacts on your cashflow, monthly mortgage, and when you actually start paying. If you’re upgrading from an HDB or planning your first big property move, understanding the difference could save you thousands.

In this guide, we break down deferred payment vs progressive payment Singapore style — with real-life examples, updated insights, and no confusing jargon. Let’s find the one that fits your budget best.

What’s the Difference Between Deferred and Progressive Payment Schemes?

Both Deferred Payment Scheme (DPS) and Progressive Payment Scheme (PPS) are ways to pay for your new launch condo or EC in Singapore — but they work very differently.

Think of DPS as “pay later, breathe now”, while PPS is more of a “pay-as-you-build” approach. Knowing which suits your needs can make or break your cashflow strategy.

Let’s break it down by buyer type

Which scheme suits different buyer profiles (first-timer, upgrader, investor)?

🏠 First-time buyers

- PPS is the default for most new launches.

- You make payments in stages — ideal if you’re not holding another property or loan.

- Mortgage starts small and scales up gradually.

Good to know: Most banks in Singapore support PPS financing. You can compare rates from DBS, UOB, and OCBC easily through a mortgage broker.

🔄 HDB upgraders

- DPS is often preferred here — you pay 20% upfront and defer your bank loan until the EC gets TOP.

- No need to manage two mortgages at once while selling your flat.

- Best used when upgrading timelines are tight.

📈 Property investors

- PPS may offer a lower entry price (since DPS units come with a premium).

- But DPS gives you the advantage of holding your capital elsewhere while the property builds.

How do the payment structures affect risk and flexibility?

Compare how Deferred and Progressive Payment Schemes affect cashflow, interest exposure, and financial control in Singapore’s property market.

Deferred Payment Scheme (DPS) vs Progressive Payment Scheme (PPS): Key Differences for Singapore Property Buyers

| Key Factor | Deferred Payment Scheme (DPS) | Progressive Payment Scheme (PPS) |

|---|---|---|

| Loan Repayment Start | After TOP | During construction (in stages) |

| Cashflow Flexibility | Higher – more time to save | Lower – payments begin earlier |

| Interest Accumulation Timeline | Delayed (may face higher future rates) | Starts earlier (can lock in current rates) |

| CPF Usage | Deferred until loan kicks in | Used progressively during build |

| Property Price | Slight premium (~2–3% more) | Usually cheaper upfront |

| Risk Exposure | Interest rate fluctuation risk | Early repayment risk, especially for upgraders |

Why do developers offer both—and which is more commonly available?

- PPS is the default for nearly all under-construction condos in Singapore.

- DPS is limited to specific EC projects that are near completion (or ready-built).

- Developers offer DPS to attract HDB upgraders who need time to sell their flat.

🎯 Watch out: DPS units sell out faster because they attract buyers with limited upfront cash. If you spot one, don’t hesitate too long.For more official details, check URA’s guide to buying residential property in Singapore.

Who Can Use the Deferred Payment Scheme?

Not everyone buying property in Singapore can tap on the Deferred Payment Scheme (DPS). It’s a niche offering — but if you’re eligible, it can buy you valuable breathing space.

Let’s break down who qualifies, what type of property it applies to, and when it actually makes sense to use it.

Is DPS available for both ECs and private condos?

Short answer: mostly ECs, not all condos.

DPS is typically offered for Executive Condos (ECs), especially those that are near completion or already built. It’s very rare to find it available for brand new, under-construction private condos in Singapore — unless the developer specifically offers it as part of a limited promo.

Why? Because banks disburse loans based on construction milestones, and most developers prefer the standard Progressive Payment Scheme for smoother cashflow.

💡 Tip: Check with your mortgage broker before shortlisting projects. They’ll know which developments are DPS-eligible in real-time.

How to tell if your EC project offers DPS before applying

Here’s how you can check before submitting a booking:

✅ Look out for “Deferred Payment Scheme available” in developer ads or brochures

✅ Ask the property agent or developer sales team directly

✅ Cross-check with a mortgage consultant — they’ll confirm the payment scheme and advise on next steps

✅ DPS is more common for ECs within 6–12 months of Temporary Occupation Permit (TOP)

And if you’re eyeing a specific EC? You can also browse recent transactions via URA’s residential property transaction search tool to see which projects are nearing completion.

When HDB upgraders should (and shouldn’t) consider DPS

DPS is practically made for HDB upgraders who need time to:

- Sell their current flat

- Avoid overlapping loans

- Stretch their CPF and cashflow

- Defer mortgage payments while managing renovation or moving costs

But it’s not always the best option. You should avoid DPS if:

🚫 You can comfortably handle staged payments under PPS

🚫 You’re buying purely for investment and want the lowest entry price

🚫 The developer charges a heavy premium for DPS units

📊 Need help comparing your costs? Use our mortgage loan repayment calculator to simulate both payment schemes side-by-side.

Cashflow Implications: How Your Monthly Finances Are Affected

Choosing between the Deferred Payment Scheme (DPS) and the Progressive Payment Scheme (PPS) isn’t just about preference — it’s about how your monthly budget will look for the next few years.

Here’s how each scheme can impact your cashflow, CPF usage, and flexibility — especially if you’re upgrading from an HDB flat.

Which scheme eases short-term financial pressure better?

✅ DPS wins this round — hands down.

With Deferred Payment, you only need to fork out the initial 20% (5% booking fee + 15% upon signing), and you won’t start repaying your home loan until the EC receives its Temporary Occupation Permit (TOP). That gives you a 2–3 year runway with zero monthly instalments.

In contrast, PPS begins home loan disbursements and mortgage repayments in phases — starting as early as 6–9 months from booking. You’ll be paying while the property is still being built.

🧠 Expert Tip: If you’re cash tight or have other ongoing financial commitments, DPS can free up your monthly budget — giving you time to rebalance before repayments kick in.

How your CPF and savings are used differently

Under PPS, your CPF and cash get drawn down early:

- You’ll start using your CPF Ordinary Account to pay for construction stage payments

- Monthly bank loan instalments begin before TOP

- Any shortfall must be covered in cash upfront

But with DPS, your CPF remains untouched until your loan starts at TOP — which can be 2 to 3 years away. That means:

✅ More time to top up your CPF OA

✅ Less financial pressure from day one

✅ Easier planning if you’re also budgeting for renovations or furnishing

🔍 Want to see how your CPF and loan repayments stack up? Try our mortgage loan repayment calculator to simulate both options.

Can you “buy time” with DPS to sell your HDB later?

Yes — and that’s one of DPS’s biggest advantages for upgraders.

If you’re transitioning from an HDB flat to an EC, you’ll need to sell your flat within 6 months of collecting your new keys. With PPS, your mortgage begins way earlier — sometimes while you’re still living in your old home.

But with DPS, you don’t need to rush your HDB sale. Because your new mortgage starts only at TOP, you have:

⏳ Time to get a better resale price

🛠️ Time for minor renovations or touch-ups

😌 Less financial stress from overlapping housing costs

📌 Just remember: You’ll still need to meet CPF usage limits and loan eligibility criteria. It’s best to speak to a mortgage advisor early if you’re juggling two properties

Mortgage Structure: How Each Scheme Impacts Your Loan

Beyond just cashflow, the Deferred Payment Scheme (DPS) and Progressive Payment Scheme (PPS) affect how your mortgage loan is structured, how interest is charged, and what your future options look like for refinancing, TDSR, and more.

If you’re serious about planning ahead — or hoping to refinance after a few years — this section is for you.

When does interest actually start building up?

Under Progressive Payment, your bank disburses the home loan in stages as construction progresses. That means interest starts accruing almost immediately — first on a small portion of the loan, then increasing as more is drawn down.

With DPS, the full loan is disbursed only after Temporary Occupation Permit (TOP), so you pay no interest until that point. However, that doesn’t necessarily save you money — you may end up with a higher loan amount if the purchase price under DPS is inflated by 2–3%.

If you’re comparing monthly payments across both schemes, use our mortgage loan repayment calculator to see the actual difference.

Will DPS affect your loan tenure, TDSR, or refinance options?

Your loan tenure stays the same regardless of scheme — typically capped at 30 years for private properties or 25 years for HDB-linked loans.

But here’s what changes:

- TDSR (Total Debt Servicing Ratio) calculations are done at the point of loan approval. If you opt for DPS, you may delay that process slightly, giving yourself time to clear other debts or boost income.

- Refinancing under DPS can be tricky, especially during the deferred period. Most banks only allow refinancing after loan disbursement — so you can’t reprice or refinance until after TOP.

For better clarity, it’s worth comparing rates and refinancing flexibility across different banks. You can check updated packages from DBS, OCBC, or UOB through a licensed mortgage broker.

Why bridging loans matter — and when to avoid them

A bridging loan is a short-term facility that helps buyers cover their new property downpayment while waiting for proceeds from their HDB sale. It’s often used by upgraders who opt for PPS and don’t have immediate liquidity.

However, with DPS, this issue is often avoided entirely.

Since your loan (and full payment) is deferred, you have time to sell your flat, settle CPF refunds, and use the cash to fund your new home without needing a bridging loan at all.

That said, bridging loans may still be necessary if:

- You’re buying under PPS and haven’t sold your HDB

- You want to secure a unit before receiving cash from your existing property

- You’re unable to align the sale and purchase timelines perfectly

Avoid bridging loans unless absolutely necessary — they come with higher interest rates and strict repayment windows. Always work with a mortgage advisor to assess whether you can plan around them.

Real Buyer Examples: DPS vs PPS for a $1M EC

Still unsure which payment scheme fits you? Let’s walk through two realistic buyer profiles — both purchasing a $1 million Executive Condo (EC) — and see how Deferred Payment Scheme (DPS) and Progressive Payment Scheme (PPS) play out in real life.

Same property. Two paths. Very different experiences.

Buyer A (DPS): Lower stress, but higher long-term cost

Daniel and Amanda are HDB upgraders. Their flat isn’t sold yet, and they don’t want to manage two mortgages at once.

They opt for the Deferred Payment Scheme, paying 20% upfront — and no monthly instalments for the next 2.5 years. That gives them time to sell their flat, sort out CPF refunds, and save for renovation.

But the trade-off?

Their unit cost $30,000 more than PPS buyers, and they risk paying a higher mortgage rate if interest climbs before TOP.

Still, the smoother cashflow and breathing space made DPS the right call for their situation.

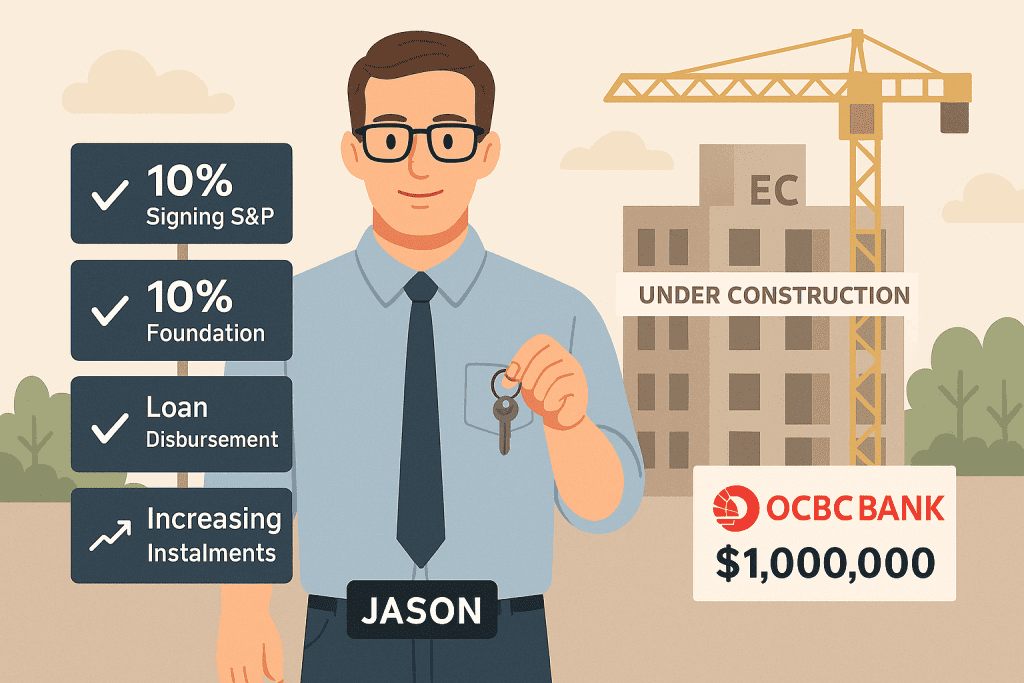

Buyer B (PPS): More payments now, but better interest control

Now meet Jason, a single buyer with no other property and stable income. He chooses PPS, locking in a unit at the base launch price of $1 million.

Within the first year, he starts paying as the EC is built:

- 10% after signing the S&P

- Another 10% as foundation completes

- Loan disbursements start within 9 months

- Monthly instalments slowly increase as construction progresses

By TOP, Jason has already paid off a decent portion of his loan. Even better — he secured a competitive fixed rate from OCBC and avoided the DPS premium.

PPS worked in his favour because he could handle the early payments and wanted interest rate certainty from day one.

What your cashflow graph looks like under each scheme

Under DPS, you’ll see a long flat line — minimal payments for years, then a sharp jump post-TOP. It’s smooth sailing at the start, but can feel steep later.

Under PPS, the graph rises gradually — smaller monthly outflows begin early, scaling as construction progresses. It requires planning, but spreads the financial load.

To see which model fits your budget, try out our mortgage loan repayment calculator. You can compare both schemes side-by-side and figure out how each path impacts your monthly finances.

Pros and Cons: The Real Trade-Offs You Should Consider

The Deferred Payment Scheme (DPS) can feel like a life-saver — especially if you’re managing an HDB sale or tight on cash. But the flexibility comes with strings attached.

Before you sign anything, here’s what you really need to weigh.

DPS Pros – Delay payments, sync with flat sale, more buffer

- No mortgage till TOP – You only pay 20% upfront, and your loan starts later. That means no pressure to juggle two mortgages.

- Perfect for HDB upgraders – You get time to sell your flat, refund CPF, and plan renovations.

- More breathing space – You can save, invest, or just get through transition costs without draining your cash.

If you’re in-between properties or your CPF is still tied up, DPS can be a practical short-term buffer.

DPS Cons – Higher price, fewer choices, long wait

- 2–3% price premium – Developers usually mark up DPS units. You’re paying more for the flexibility.

- Limited availability – Not all projects offer DPS, and those that do often release fewer units under it.

- Higher rate risk – If interest rates rise before TOP, you’ll be stuck with a pricier loan when the scheme ends.

And unlike Progressive Payment Scheme, you can’t lock in today’s rates — which could make refinancing harder down the road.

How to decide if DPS is truly worth the premium

Here’s a quick test:

- You haven’t sold your HDB? → DPS might save you a financial headache

- You’re tight on CPF/cash? → DPS buys you time

- But if you’ve got no major commitments and want to lock in the best mortgage rates in Singapore, PPS could be cheaper in the long run

Need help doing the math? Use our mortgage loan repayment calculator or speak with a mortgage advisor to run the numbers for both options before you commit.

FAQs – What Buyers Are Asking

Still unsure about the finer details of Deferred Payment Scheme (DPS) vs Progressive Payment Scheme (PPS)? You’re not alone. These are some of the most common questions homebuyers in Singapore are asking this year.

Can you switch payment scheme after booking your EC?

Usually, no. Once you’ve selected your payment scheme and signed the Sale & Purchase Agreement (S&P), the developer locks it in.

If you want DPS, you’ll need to confirm its availability before booking. Not all projects offer it, and those that do often allocate only a limited number of units.

💡 Best move? Confirm with your agent and get clarity through a mortgage advisor before paying the option fee.

Do banks charge different rates under DPS vs PPS?

Yes — and it depends on timing.

With PPS, you start your mortgage early, which means you can lock in current mortgage interest rates in Singapore — whether it’s a fixed or SORA-pegged rate.

With DPS, your loan only kicks in after TOP. That means your rate will depend on market conditions 2–3 years later. If interest rates rise in that time, you may end up with a higher cost of borrowing.

To compare rates today, check out packages from DBS, UOB, or OCBC and assess what’s best for your situation.

Will choosing DPS affect stamp duty or CPF grants?

No, the payment scheme doesn’t affect stamp duty or CPF housing grants.

- Buyer’s Stamp Duty (BSD) is based on your property price — regardless of whether you choose DPS or PPS. You can estimate yours using our BSD calculator.

- CPF grants (like the Enhanced Housing Grant or Family Grant for ECs) are based on eligibility, income, and property type — not payment scheme.

However, the higher pricing under DPS may push your property value above grant ceilings in some cases. Always check with your agent or a mortgage specialist before assuming you’ll qualify.

Should You Pick Deferred or Progressive Payment?

If you’re still on the fence, don’t worry — the right choice depends entirely on your financial situation, timeline, and risk appetite.

Here’s a quick decision guide to help you figure it out.

3 quick questions to reveal which scheme suits you

Ask yourself:

- Do I need time to sell my current HDB or build up CPF savings?

→ If yes, DPS gives you breathing space. - Am I ready to start monthly payments within the next 6–12 months?

→ If yes, PPS might save you more in the long run. - Am I concerned about future interest rate hikes?

→ PPS allows you to lock in today’s mortgage rates and avoid future spikes.

If you answered “yes” to the first question and “no” to the others, DPS is likely your safer bet. Otherwise, PPS could help you save more overall.

When to prioritise cashflow over long-term interest savings

You should prioritise cashflow (i.e. go with DPS) if:

- You’re upgrading from an HDB flat and need to wait for your sale proceeds

- You want to avoid bridging loans and CPF refund stress

- You need time to build reserves for renovation or furnishings

Go with PPS if:

- You’re financially ready and want to avoid the DPS property price premium

- You prefer interest rate certainty and better long-term cost control

- You’re a first-time buyer without overlapping housing costs

Get advice before locking in — a small step that saves big

Choosing between Deferred Payment Scheme vs Progressive Payment Scheme in Singapore is more than just timing — it’s about how your home loan fits into your full financial picture.

A quick chat with a Singapore mortgage broker can help you:

- Compare rates across major banks like DBS, UOB, and OCBC

- Assess your loan eligibility and CPF use

- Avoid costly mistakes before you commit to a unit

Don’t guess your way through a six-figure decision. Know your numbers, weigh your options, and make the scheme work for you — not the other way around.

Final Thoughts: Choose the Right Payment Scheme for Your Property Goals

Understanding the real impact of Deferred vs Progressive Payment helps you avoid costly mistakes and make smarter, stress-free buying decisions.

Both Deferred Payment Scheme (DPS) and Progressive Payment Scheme (PPS) offer unique advantages — but choosing the right one depends on your personal cashflow, timeline, and financial readiness.

- Go with DPS if you need short-term breathing room, especially as an HDB upgrader or buyer with limited upfront cash.

- Choose PPS if you prefer full cost transparency, better interest rate control, and are financially prepared to start repayments earlier.

If you’re still unsure, don’t go it alone.

Speak to a Singapore Mortgage Expert Today

Book a free consultation with a licensed mortgage broker in Singapore to:

- Compare rates from DBS, UOB, OCBC, and more

- Explore refinance options or HDB loan alternatives if you’re upgrading

- Get personalised advice based on your CPF, income, and property timeline

Or run your own numbers with our mortgage loan repayment calculator to see what fits your budget.

Your property decision isn’t just about the home — it’s about the plan behind it. Make it count.