Thinking about buying your dream home in Singapore and wondering how to apply for a Citibank mortgage loan? You’re definitely not alone. With so many banks and loan packages out there, it can be confusing to know where to start. That’s where this guide comes in.

We’ll walk you through the entire process—from eligibility requirements to application steps—so you know exactly what to expect when you apply for a Citibank mortgage in 2025.

We’ll also cover the latest interest rates, tips for refinancing, and how Citibank’s home loan packages stack up against other banks.

Whether you’re a first-time buyer or thinking of upgrading, this guide is designed to make the journey as smooth and stress-free as possible. Let’s get started on your path to homeownership in Singapore!

Citibank Home Loan Eligibility Requirements

Before you apply for a Citibank mortgage loan in Singapore, it’s important to know if you meet the bank’s eligibility requirements. This ensures a smoother process and avoids unnecessary delays.

What are the minimum income and age requirements for applicants?

Citibank typically requires applicants to be at least 21 years old at the time of application. For income, a minimum gross monthly income of around S$3,000 is recommended—though this can vary depending on property type and loan amount.

Minimum Eligibility Requirements for Citibank Mortgage Loan Singapore

| Eligibility Criteria | Details |

|---|---|

| Minimum Age | 21 years old |

| Minimum Gross Monthly Income | S$3,000 (indicative, may vary) |

| Credit History | Good credit profile helps secure better rates |

Even if you meet the minimum income, having a solid credit score can improve your chances of getting approved and help you secure more competitive home loan interest rates in Singapore.

Can foreigners apply for a Citibank home loan in Singapore?

Yes, foreigners can apply for a Citibank home loan. However, they may face stricter credit checks and a lower Loan-to-Value (LTV) ratio than Singapore Citizens or PRs. This is standard practice across most banks in Singapore.

Pro Tip: If you’re a foreigner, it’s a good idea to consult with a Citibank mortgage advisor early to understand any additional requirements.

For general guidance on eligibility and LTV ratios, you can refer to MoneySense or CPF Housing Loan Eligibility resources.

What documents are needed for a smooth application process?

Having the right documents ready can speed up your mortgage application and reduce delays. Typically, you’ll need:

- NRIC or Passport (for foreigners)

- Latest 3 months’ payslips

- CPF contribution history

- Latest IRAS Notice of Assessment

- Option to Purchase (OTP) or Sale & Purchase Agreement

- Property details and valuation report (if available)

Being well-prepared ensures that your mortgage approval process goes as smoothly as possible. If you’re unsure about any document, reach out to a Citibank mortgage advisor for help.

Read our latest guide on mortgage lenders with the lowest rates in Singapore to find the best deal for your home loan.

Step-by-Step Guide to Applying for a Citibank Mortgage

Applying for a Citibank mortgage loan in Singapore doesn’t have to feel overwhelming. Here’s a straightforward, step-by-step guide to help you navigate the application process with ease and confidence.

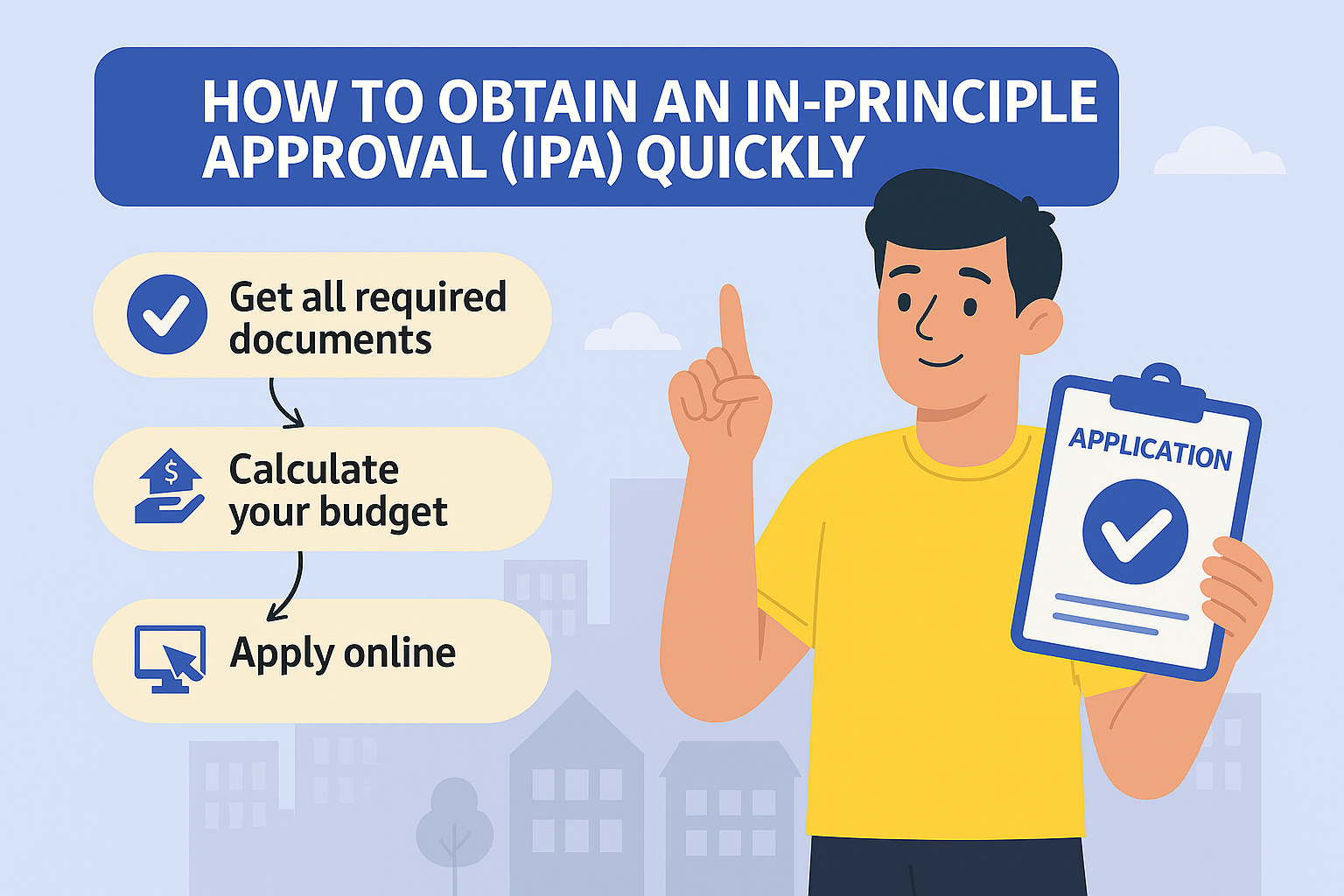

How to obtain an In-Principle Approval (IPA) quickly

The In-Principle Approval (IPA) is a crucial first step in the home loan process. It’s essentially Citibank’s way of telling you how much you can borrow before you commit to a property. Here’s how to get it quickly:

- Submit your application online or through a Citibank mortgage advisor.

- Provide key documents like income statements, CPF contributions, and your latest Notice of Assessment.

- Double-check all your documents to avoid delays.

Once you’ve submitted everything, Citibank usually provides an IPA decision within 3 to 5 working days. Having an IPA in hand makes it easier to shop for a home with confidence.

Pro Tip: Getting an IPA doesn’t commit you to any particular property yet, but it gives you a solid idea of your borrowing limit. That means you can negotiate better with sellers and agents.

For more guidance on preparing documents and calculating your loan eligibility, check out our mortgage loan calculator.

What is the typical loan approval timeline and disbursement process?

Once you’ve signed the Option to Purchase (OTP), you’ll need to submit a full loan application to Citibank. Here’s what to expect:

- Loan Approval Timeline: Typically, it takes around 1 to 2 weeks for Citibank to process and approve the loan after receiving all the necessary documents.

- Loan Offer Letter: Once approved, Citibank will issue a formal offer letter with details on your loan amount, interest rate, and repayment terms.

- Acceptance and Disbursement: After you accept the offer, funds are usually disbursed directly to the seller’s solicitor or your appointed lawyer within 1 to 2 weeks.

Delays usually happen when supporting documents are incomplete or missing. To avoid this, stay in touch with your mortgage broker or bank officer, and make sure you submit everything promptly.

How to track your application status online

Citibank makes it easy to track your application status online through their secure customer portal. Here’s how:

- Log in to your Citibank Online account.

- Go to the Mortgage Loan Application section.

- Check your loan application status, which is updated regularly.

- For any questions, contact Citibank’s mortgage support team directly.

If you’re using a mortgage broker, they can also help you stay informed and liaise with the bank on your behalf.

Here’s a tip for you: Staying proactive with your application status can help you catch any issues early, like missing documents or signature requirements, which could delay your approval.

Citibank Mortgage Loan Interest Rates in 2025

Understanding the latest Citibank mortgage loan interest rates in Singapore is crucial for making informed decisions. As of June 2025, Citibank offers a variety of fixed and floating rate packages tailored to different needs.

What are the latest fixed and floating rate packages available?

Citibank’s offerings are designed to give you flexibility whether you prefer rate certainty or the potential for savings when interest rates fluctuate.

Latest Citibank Mortgage Loan Rates in (January 2026)

| Package Type | Indicative Rate | Notes |

|---|---|---|

| 1-Year Fixed Rate | 1.90% p.a. | For Citigold clients; reverts to prevailing rates after the first year. |

| 2-Year Fixed Rate | 1.90% p.a. | For Citigold clients; reverts to floating rates after two years. |

| 3M Compounded SORA Floating Rate | 1.88% p.a. (SORA + 0.35% spread) | Adjusts quarterly; may vary with market conditions. |

Rates are indicative as of June 2025 and subject to change. Always consult a Citibank mortgage advisor for the most current offers.

My honest opinion is that fixed rate packages are great if you value stability, while floating rates can offer savings when market rates decline—but be prepared for upward adjustments too.

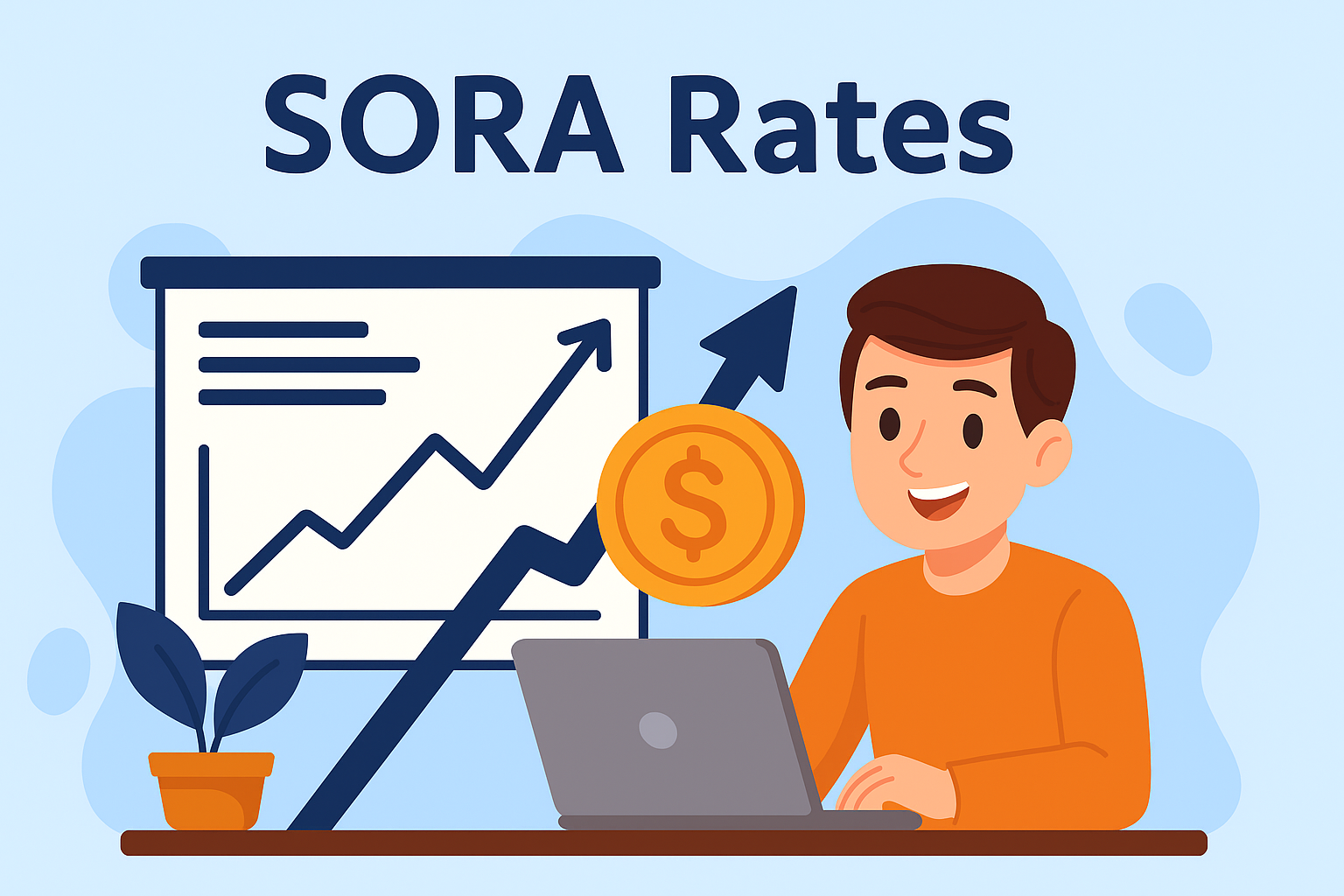

How does the Compounded SORA benchmark affect your loan?

The Singapore Overnight Rate Average (SORA) is the new benchmark for floating rates in Singapore. As of mid-2025, the 3-month SORA rate is approximately 2.63% (source). Citibank’s floating rates are structured as SORA plus a fixed spread, commonly around 0.60% p.a.

This means your interest rate—and hence your monthly repayments—will adjust based on SORA market movements. It can help you save when rates drop, but your repayments might increase if rates rise. It’s a good idea to consider your financial comfort zone before choosing a floating rate package.

What are the exclusive rates and perks for Citigold clients?

Citigold clients enjoy special perks that make financing your home even more attractive. Here’s what you can expect:

- Preferential Rates: Lower spreads on both fixed and floating packages compared to standard rates.

- Exclusive Promotions: Access to limited-time offers, investment bundles, or rewards. Learn more on Citigold’s official site.

- Dedicated Relationship Manager: Personalised financial advice and priority service throughout the loan process.

To qualify for Citigold status, maintain a minimum combined average monthly balance of S$250,000 in eligible accounts. If you’re planning to finance a new home, ask your Citibank mortgage advisor if Citigold benefits could work for you.

Refinancing Your Mortgage with Citibank

Thinking about refinancing your home loan? Whether you’re aiming to lower your monthly payments, switch to a more attractive package, or tap into equity, Citibank mortgage refinancing in Singapore offers a variety of solutions to meet your needs in 2025.

What are the key benefits of refinancing with Citibank?

Refinancing with Citibank can help homeowners achieve financial flexibility and potentially save on interest payments. Here are some key benefits:

- Competitive Interest Rates: Citibank offers attractive refinancing rates, including fixed and floating rate packages, to help you manage your budget.

- Flexible Loan Packages: Choose between fixed rates for stability or floating rates linked to SORA for potential savings.

- Interest-Offset Features: Allows you to offset your mortgage interest with savings, helping you pay less over time.

Refinancing is not just about interest rates—it’s about aligning your loan with your current financial goals. A Citibank mortgage advisor can help you evaluate your options and pick the best package for your situation.

What are the current refinancing rates and packages in 2025?

Citibank’s refinancing rates are aligned with its regular mortgage packages. For the latest fixed and floating rate options, refer to our complete Citibank home loan rates guide.

That said, Citibank may offer exclusive refinancing perks such as legal fee subsidies or interest-offset features, especially for high-loan quantum clients.

Exclusive Features for Refinancing Clients (2025)

| Feature | Details |

|---|---|

| Legal Fee Subsidy | Up to $2,000 subsidy for refinancing from another bank |

| Interest-Offset Savings Account | Reduces interest payable based on account balance |

| Flexible Lock-in Options | Choice of 2- or 3-year fixed rates with partial prepayment flexibility |

If your current rate is above 3%, you may benefit from refinancing, especially if you’re eligible for a Citibank interest-offset package.

How does the interest-offset feature work for refinancing customers?

One of Citibank’s standout features is the Home Saver Interest Offset Account, designed to help you reduce interest costs while keeping your funds accessible. Here’s how it works:

- You can link a savings account to your mortgage, with a portion of your balance offsetting the interest charged on your loan.

- The offset amount typically reduces your effective interest rate, lowering your monthly repayments.

- You retain full access to your linked savings account, providing both flexibility and savings potential.

Pro Tip: If you regularly keep savings parked in your account, the interest-offset feature can be a smart way to manage your cash flow while reducing overall mortgage costs.

For more details on this feature, speak with a Citibank mortgage advisor to see if it fits your financial strategy.

Citibank Home Loans for Buildings Under Construction (BUC)

Buying a property that’s still being built? With Citibank’s home loans for Buildings Under Construction (BUC), you can finance your purchase even before the project is completed. Here’s what you need to know to make an informed choice.

What are the loan options for BUC properties in Singapore?

Citibank offers flexible loan options specifically tailored for BUC properties, making it easier for buyers to secure financing early in the homebuying process. Here’s an overview:

- Progressive Payment Scheme: This is the most common structure for BUC loans in Singapore, allowing you to make payments in stages as the construction progresses.

- Fixed and Floating Rate Packages: You can choose between stable fixed-rate packages (often 1-2 years) or floating rates pegged to SORA for potential savings.

Citigold Exclusive Packages: Enjoy preferential rates and dedicated service if you qualify as a Citigold client.

Are there lock-in periods or special terms for BUC loans?

Yes, BUC loans from Citibank typically come with a lock-in period ranging from 2 to 3 years. This means if you refinance or pay off your loan early during this period, you might incur a penalty fee.

Here’s a quick summary:

Summary of Citibank BUC Loan Features and Lock-In Terms (2025)

| BUC Loan Feature | Details |

|---|---|

| Lock-In Period | Usually 2 to 3 years |

| Early Repayment Penalties | Typically 1.5% of the outstanding loan amount |

| Progress Payments | Payments made at key construction milestones |

Pro Tip: Always clarify the lock-in period details with a Citibank mortgage advisor before committing, as it could affect your refinancing flexibility later on.

How do interest rates differ for BUC loans compared to completed properties?

Interest rates for BUC loans can sometimes be slightly higher than those for completed properties. This is because banks take on more risk financing a property that isn’t fully built. As of June 2025:

- Fixed Rates for BUC: Typically start around 2.85% p.a. for Citigold clients.

- Floating Rates for BUC: Usually SORA + 0.60% spread, aligning with current market rates.

Keep in mind that BUC loans follow the progressive payment scheme, which means you’ll only pay interest on the disbursed portion, not the entire loan amount upfront. This can ease your cash flow during construction.

Expert Insight: Even a small difference in rates can add up over time. It’s wise to compare your options using a mortgage calculator to understand your total cost of borrowing.

For the latest updates on progressive payments and loan structures, check out HDB’s payment website.

Fees and Charges for Citibank Home Loans

Understanding the fees and charges for Citibank home loans in Singapore is key to avoiding surprises and budgeting effectively. Let’s dive into what you can expect.

What are the partial and full redemption penalties?

If you decide to repay your mortgage early—either partially or fully—Citibank typically imposes a redemption penalty during the lock-in period. This is a standard feature in most home loan agreements in Singapore.

Citibank Home Loan Partial and Full Redemption Penalties (2025)

| Redemption Type | Penalty |

|---|---|

| Partial Redemption | 1.5% of the amount redeemed (during lock-in period) |

| Full Redemption | 1.5% of the outstanding loan amount (during lock-in period) |

After the lock-in period ends, you can usually make partial or full repayments without penalties. Always double-check with your Citibank mortgage advisor before making early payments to avoid unexpected costs.

What legal and valuation fees should borrowers expect?

In addition to your monthly repayments, you’ll need to account for legal and valuation fees:

- Legal Fees: Usually range between S$2,500 and S$3,000, depending on the law firm and loan package.

- Valuation Fees: Typically range from S$350 to S$500, depending on the property’s market value.

These fees cover the cost of legal paperwork and ensuring your property’s valuation is up to date. For more details on budgeting, use our mortgage calculator to estimate your total costs.

Are there any fee waivers or special offers for Citigold clients?

Citigold clients can often benefit from exclusive promotions and fee waivers, including:

- Legal Subsidies: Some packages include partial or full subsidies on legal fees.

- Valuation Fee Waivers: Certain promotions waive the valuation fees entirely.

- Exclusive Citigold Perks: Dedicated relationship managers, financial advice, and occasional welcome rewards.

Pro Tip: These perks vary by market conditions. Speak to your Citibank mortgage advisor to find out what’s currently available.

You can also visit the Citigold official page for the latest offers.

Using Citibank’s Mortgage Tools and Resources

Navigating the home loan process is easier when you know which tools and resources are available. Citibank offers a range of helpful options that can make your mortgage journey smoother and more informed.

How to use the Citibank mortgage loan repayment calculator effectively

Before you commit to a Citibank mortgage loan, it’s wise to estimate your monthly payments. Citibank’s mortgage loan repayment calculator helps you plan your budget confidently by factoring in your loan amount, tenure, and interest rate.

Here’s how to get the most out of it:

- Input Loan Amount: Enter your desired loan principal amount.

- Select Tenure: Choose your loan term, typically ranging from 10 to 30 years.

- Interest Rate: Input the indicative rate—check current rates on our home loan rates page.

- Calculate: Click “Calculate” to get an estimate of your monthly payments, including principal and interest.

Pro Tip: Use the calculator regularly, especially if you’re comparing different Citibank home loan packages or considering refinancing.

You can access Ace Mortgage’s own mortgage calculator for additional comparison and planning features.

What is the Home Saver Interest Offset Account?

Citibank’s Home Saver Interest Offset Account is a unique feature that helps you reduce the overall interest you pay on your mortgage. Here’s what makes it valuable:

Key Features of Citibank Home Saver Interest Offset Account

| Feature | Details |

|---|---|

| Interest Offset | A portion of your savings in the offset account reduces the interest payable on your mortgage. |

| Accessibility | Your funds remain accessible, giving you financial flexibility. |

| Benefit | Helps lower your effective interest rate, reducing total interest payments over time. |

Expert Insight: If you tend to maintain a higher savings balance, this account can be a smart way to reduce your interest burden without sacrificing liquidity.

For a more detailed explanation, speak to a Citibank mortgage advisor or explore how offset accounts work at MoneySense.

How to connect with Citibank’s mortgage advisors and support team

Whether you’re just starting your home loan journey or need help with refinancing, Citibank’s dedicated mortgage advisors can guide you every step of the way.

Here’s how to get in touch:

- Visit a Citibank Branch: Drop by any Citibank branch in Singapore.

- Schedule an Appointment: Contact their mortgage hotline or arrange a callback through the Citibank website.

- Speak to an Advisor: Work with a Singapore mortgage broker who can liaise with Citibank on your behalf and help you compare rates.

Pro Tip: Don’t hesitate to ask your advisor about the latest Citibank mortgage loan packages or refinancing deals. Staying updated can save you thousands over the life of your loan.

Frequently Asked Questions About Citibank Home Loans

It’s natural to have questions when you’re planning to take on a Citibank home loan. Here, we tackle some of the most common questions to help you make confident decisions.

What is the Loan-To-Value (LTV) ratio and why does it matter?

The Loan-To-Value (LTV) ratio refers to the maximum amount you can borrow as a percentage of your property’s appraised value. For example, if your property is valued at S$1 million and the LTV is 75%, you can borrow up to S$750,000.

In Singapore, LTV ratios are regulated by the Monetary Authority of Singapore (MAS). For most buyers:

- First housing loan: Up to 75% LTV

- Second housing loan: Up to 45% LTV

- Third housing loan: Up to 35% LTV

A lower LTV means a higher down payment requirement, so it’s essential to plan your finances carefully. For a deeper understanding, check out our mortgage loan repayment calculator to estimate your payments.

Expert Tip: Foreigners and buyers with existing loans may face stricter LTV limits—always check with your Citibank mortgage advisor for specific guidelines.

What is the significance of the Option to Purchase (OTP)?

The Option to Purchase (OTP) is a legal document that gives you the exclusive right to buy the property from the seller, usually valid for 14 to 21 days. During this time, you can secure financing (like your Citibank home loan) and complete the necessary checks.

Key things to know:

- You typically pay an option fee (1% of the purchase price) to secure the OTP.

- If you decide to proceed, you exercise the OTP by signing it and paying the balance of the deposit (usually 4%).

- If you don’t proceed, you forfeit the option fee.

Pro Tip: Getting an In-Principle Approval (IPA) from Citibank before signing the OTP can save time and reduce uncertainty.

How does fire insurance integrate into your home loan?

Fire insurance is mandatory for all HDB flats and recommended for private properties. It protects your property against structural damage due to fire and is often a condition for home loan disbursement.

Here’s how it fits into your Citibank home loan:

- Requirement: Most banks, including Citibank, require you to have valid fire insurance before they disburse your loan.

- Provider: You can choose from various insurers, including those recommended by Citibank.

- Annual Premium: Usually affordable, around S$50–S$100 depending on the property’s size and value.

Expert Tip: Fire insurance only covers the building structure, not your contents. Consider getting a separate home insurance policy for better protection.

For more on how this fits into your home loan planning, speak to a Citibank mortgage advisor or visit MoneySense.

Contacting Citibank for Mortgage Assistance

Once you’re ready to take the next step with your Citibank mortgage loan, getting in touch with the right support team is crucial. Here’s how to easily connect with Citibank’s mortgage advisors and access help when you need it.

How to reach Citibank’s mortgage advisors in Singapore

Citibank offers several convenient ways to reach their experienced mortgage advisors:

- Direct Contact: Visit a Citibank branch or call their mortgage hotline for personalized advice.

- Online Enquiry: Submit a contact form on Citibank’s official website to request a callback.

- Mortgage Brokers: Work with a Singapore mortgage broker who can liaise with Citibank on your behalf, answer questions, and help you compare the best loan packages.

Expert Tip: Having a mortgage broker on your side can streamline the application process and help you secure the best rates.

What are the operating hours and hotline numbers?

Citibank’s mortgage advisors are generally available during standard banking hours, but it’s always good to double-check for the most current details.

Citibank Singapore Mortgage Hotline Numbers and Operating Hours

| Service Channel | Operating Hours | Hotline Number |

|---|---|---|

| Mortgage Hotline | Mon–Fri: 9am–6pm | +65 6238 8833 |

| Branches | Varies by location | Refer to Citibank branch directory |

| Online Enquiry | 24/7 Submission | — |

Note: Hotline hours may vary on public holidays—always double-check with the Citibank official site

Where are Citibank’s key branches located in Singapore?

Citibank has several conveniently located branches where you can meet with a mortgage advisor face-to-face. Some key branches include:

- Citibank Orchard Branch: 391A Orchard Road, #12-01 Ngee Ann City Tower A, Singapore 238873

- Citibank Raffles Place Branch: 3 Raffles Place, #02-01 Bharat Building, Singapore 048617

- Citibank Holland Village Branch: 263 Holland Avenue, Singapore 278987

For the full list of branches and their operating hours, refer to the Citibank Singapore branch directory.

Pro Tip: Always call ahead or check online to confirm branch hours before visiting.

Conclusion: Your Path to a Citibank Mortgage Loan in Singapore

Buying a home or refinancing in 2025? With the right support, applying for a Citibank mortgage loan in Singapore is easier than you think. Whether you’re figuring out how much you can borrow, comparing rates, or just exploring your options, you’re not alone.

Start by using our mortgage loan repayment calculator to estimate your monthly instalments. Need help deciding? Chat with a trusted mortgage advisor who can walk you through the process.

And if you’re ready to explore your options, check out the latest home loan rates in Singapore to see how Citibank stacks up.

Here’s to making your homeownership dreams a reality!