Thinking about buying a home in Singapore? Let’s face it — home loan rates can be confusing. With fixed, floating, and hybrid rates, banks offer all sorts of packages that sound complicated.

But here’s the good news: comparing home loan rates doesn’t have to be overwhelming. In this guide, I’ll walk you through how to compare home loan rates in Singapore, so you can find the best deal for your dream home.

Ready? Let’s get started!

Why Comparing Home Loan Rates Matters

Comparing home loan rates in Singapore isn’t just about getting the lowest headline rate — it’s about finding a loan that fits your budget and financial goals. Let’s dive into why comparing rates is so important for homebuyers.

How Rate Differences Impact Monthly Payments

Even a small difference in rates can make a big difference in your monthly payments. For example:

- A 0.1% change might not sound like much, but over a 25-year loan, it can add up to thousands of dollars.

- Lower rates mean lower monthly payments — giving you more breathing room in your budget.

Pro Tip: Use our mortgage loan calculator to see how different rates affect your repayments.

Lock-In Periods, Fees, and Penalties to Watch For

Banks often sweeten the deal with attractive rates — but there’s a catch. Watch out for:

- Lock-In Periods: Usually 2-3 years where you can’t refinance without paying a penalty.

- Early Repayment Penalties: Fees charged if you repay your loan early during the lock-in.

- Other Costs: Valuation fees, legal fees, and administrative charges that can add up.

Always read the fine print and ask the bank to explain any terms you’re unsure about.

How Small Rate Differences Can Save You Thousands

Let’s put it into perspective:

- On a $500,000 loan over 25 years, a 0.25% lower rate can save you over $17,000 in interest.

- Even small savings add up — giving you more money for renovations, savings, or investments.

Expert Tip: Comparing rates from DBS, UOB, and OCBC can reveal hidden gems. Don’t forget to check out the homepage for the latest promotions and tools to help you choose the best loan for your needs.

Quick Overview of Home Loan Rates in Singapore

Before diving into the details, here’s a quick snapshot comparing the typical fixed, floating, and hybrid home loan rates in Singapore as of recently. This overview helps you understand which rate type might suit your needs best — whether you value stability, flexibility, or a mix of both.

Snapshot Comparison of Fixed, Floating, and Hybrid Home Loan Rates (January 2026)

| Loan Type | Typical Rate Range | Best For |

|---|---|---|

| Fixed Rate | 1.40% – 2.45% | Predictable payments, budgeting |

| Floating Rate (SORA) | 1.39% – 2.77% | Potential savings, but variable payments |

| Hybrid Packages | Varies by bank | Some stability with market exposure |

Side-by-Side Comparison of Home Loan Rates

Before diving into the rates, here’s a simple table comparing fixed and floating home loan rates from DBS, UOB, and OCBC to help you make a quick side-by-side comparison.

Home Loan Rates Comparison Across Banks (January 2026)

| Bank | Fixed Rate (2-Year) | Floating Rate (SORA) | Lock-In Period | Special Promotions |

|---|---|---|---|---|

| OCBC | From 1.50% | From 1.39% | 2 years | Cash rebates for refinancing, green mortgage options |

| DBS | From 1.48% | From 1.52% | 2–3 years | Valuation subsidies, priority banking rates |

| UOB | From 1.50% | From 1.52% | 2 years | Complimentary valuations, hybrid options |

Note: Rates are indicative and subject to change. For the latest updates and package details, explore current offers from DBS, UOB, or OCBC.

Types of Home Loan Rates in Singapore

Choosing the right home loan rate can make a huge difference in your monthly payments and long-term savings. Let’s break down the three main types of rates in Singapore and what each means for you.

Fixed Home Loan Rates — When Stability Matters

Why Choose a Fixed Rate?

A fixed home loan rate means your interest rate stays the same for a set period (usually 2–3 years).

Key Features of Fixed Home Loan Rates (January 2026)

| Feature | Description |

|---|---|

| Rate Stability | Payments remain constant during lock-in |

| Lock-In Period | Typically 2–3 years |

| Rate After Lock-In | Usually reverts to floating rate |

| Best For | Budget-conscious homeowners |

Pros:

- Predictable payments for easy budgeting.

- Peace of mind — no sudden spikes in payments.

Cons:

- Often slightly higher than starting floating rates.

- Rates may revert to higher floating rates after the fixed term ends.

Floating Home Loan Rates — Flexibility and Market Movement

Why Choose a Floating Rate?

Floating rates are tied to market benchmarks like SORA, meaning they can change over time.

Key Features of Floating Home Loan Rates (January 2026)

| Feature | Description |

|---|---|

| Rate Linkage | Pegged to SORA or bank’s internal rate |

| Rate Changes | Adjusts every 1–3 months |

| Best For | Homeowners comfortable with risk |

Pros:

- Potential savings if rates drop.

- Flexibility — some packages allow switching to fixed later.

Cons:

- Rates can rise, increasing monthly payments.

- Less predictability, harder to budget.

Tip: Curious about how SORA impacts your loan? Check out our refinancing guide for strategies on managing rate changes.

Hybrid Packages — Combining Fixed and Floating Rates

Why Choose a Hybrid Package?

A hybrid package splits your loan into fixed and floating components.

Key Features of Hybrid Home Loan Rates (January 2026)

| Feature | Description |

|---|---|

| Fixed Portion | Stability for part of the loan |

| Floating Portion | Opportunity to benefit from rate drops |

| Best For | Buyers who want balance |

Pros:

- Balanced approach — some predictability plus flexibility.

- Lets you hedge against both rate hikes and drops.

Cons:

- Can be complex to understand.

- Packages vary widely by bank — read the fine print.

Pro Tip: Hybrid rates can vary significantly. For expert help, speak to a Singapore mortgage broker who can guide you to the best package for your needs.

Bank-Specific Home Loan Packages and Promotions

When it comes to comparing home loan rates in Singapore, each bank offers its own mix of packages, rates, and promotions. Let’s take a look at the latest deals from DBS, UOB, and OCBC.

DBS Home Loan Rates and Packages

Why Consider DBS Home Loans?

DBS offers competitive rates with flexible packages. Here’s what’s available this month:

Latest DBS Home Loan Rates and Packages (January 2026)

| Package Type | Rate Range | Key Features |

|---|---|---|

| Fixed Rate | From 1.48% (2-year) | Stable payments, 2–3 year lock-in. |

| Floating (SORA) | From 1.52% | Pegged to SORA, rates adjust with market. |

Perks:

- Online application discounts.

- Priority banking clients may enjoy special rates.

- Some packages offer valuation fee subsidies.

Expert Tip: Always check the lock-in period and what rate you’ll revert to after the promo ends. For more details, visit our DBS Home Loan page.

UOB Mortgage Loan Offers and Interest Rates

Why Consider UOB Home Loans?

UOB is known for promotions catering to first-time buyers and BTO homeowners.

Latest UOB Mortgage Loan Rates and Promotions (January 2026)

| Package Type | Rate Range | Key Features |

|---|---|---|

| Fixed Rate | From 1.50% (2-year) | Budget-friendly, stable payments. |

| Floating (SORA) | From 1.52% | Market-linked, potential for savings. |

Highlights:

- Complimentary property valuations on select packages.

- Hybrid packages (50% fixed + 50% floating) available.

- Flexible repayment structures for new launches.

In my opinion, UOB can be a great choice for new launches or BTO buyers, but remember that SORA rates can fluctuate so plan your budget accordingly. Explore our UOB Home Loan page for updated rates and insights.

OCBC Housing Loan Rates and Promotions

Why Consider OCBC Home Loans?

OCBC offers a range of rates and promotions for both new and resale properties.

Latest OCBC Home Loan Rates and Promotions (January 2026)

| Package Type | Rate Range | Key Features |

|---|---|---|

| Fixed Rate | From 1.50% (2-year) | Steady payments, easy budgeting |

| Floating (SORA) | From 1.52% | Flexibility to ride market trends |

Highlights:

- Cash rebates for refinancing packages.

- Green mortgage options available.

- Flexible lock-in periods on selected loans.

Remember to always compare lock-in periods and fees to avoid surprises. Check out our OCBC Home Loan page

Key Factors to Consider When Comparing Rates

When comparing home loan rates in Singapore, it’s not just about the interest rate itself. Banks also consider factors like TDSR, MSR, and CPF usage—and so should you! Let’s unpack what these mean for your home loan application.

Total Debt Servicing Ratio (TDSR) and Its Impact on Loan Eligibility

Why It Matters:

The Total Debt Servicing Ratio (TDSR) is a government regulation that caps your total monthly debt payments—including home loans, car loans, and credit cards—at 55% of your gross monthly income.

TDSR Overview for Home Loan Applicants (January 2026)

| Factor | Description |

|---|---|

| TDSR Threshold | 55% of gross monthly income |

| Includes | All debt obligations (e.g. loans, cards) |

| Affects | How much banks will lend you |

Tips for Managing TDSR:

- Pay down other debts to lower your ratio.

- Extend your loan tenure to reduce monthly payments.

Pro Tip: Unsure how the Total Debt Servicing Ratio works? Read our full guide on TDSR here to see how it can impact your home loan eligibility.

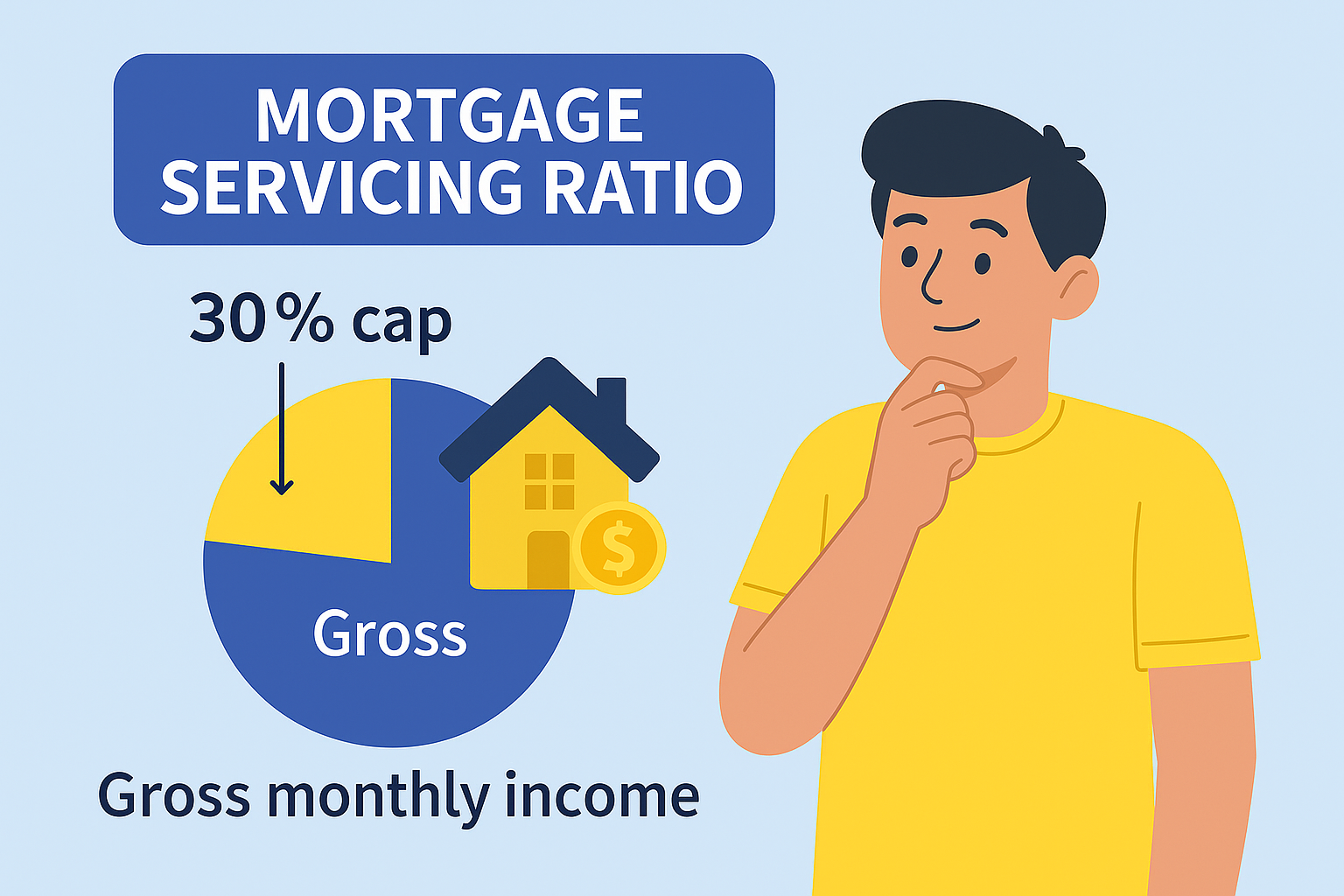

Mortgage Servicing Ratio (MSR) for HDB and EC Buyers

If you’re buying an HDB flat or an Executive Condominium (EC), the Mortgage Servicing Ratio (MSR) applies too. It limits your monthly mortgage repayments to 30% of your gross monthly income.

Key Points:

- Only applies to HDB flats and ECs, not private condos.

- Works alongside TDSR—both must be met.

- Affects the maximum loan amount you can secure.

Based on past experience, many buyers forget that grants can help reduce the effective MSR ratio. Check your eligibility on our HDB Home Loan page or speak to a mortgage specialist for tailored advice.

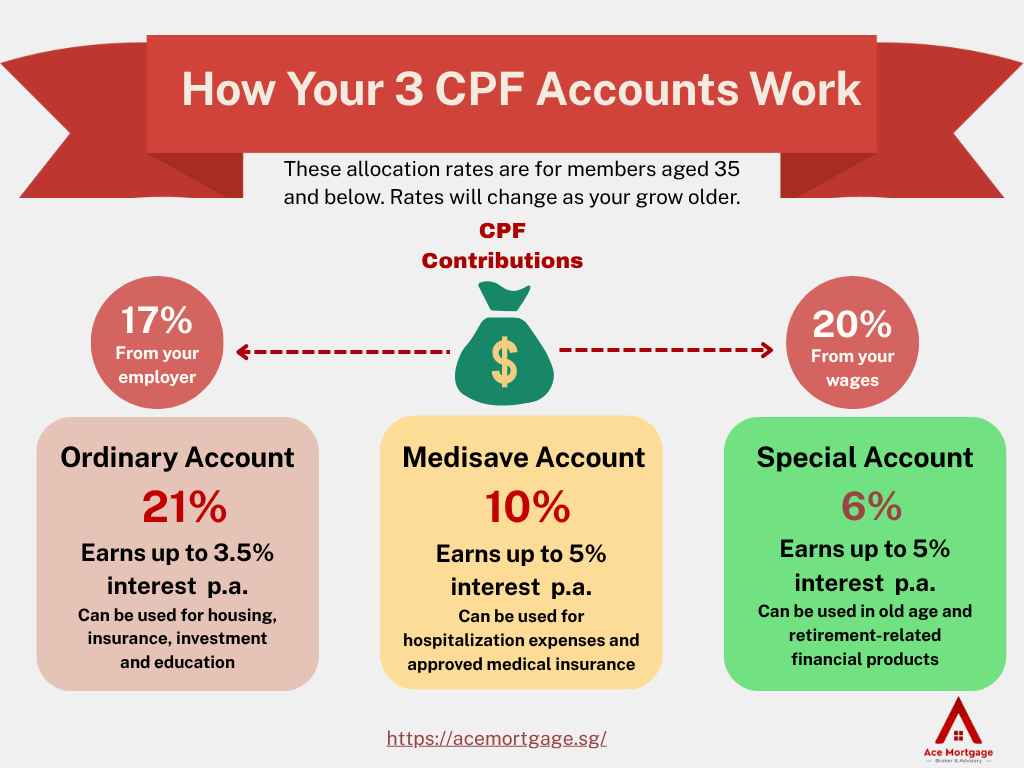

CPF Usage — Using Your CPF Ordinary Account Wisely

Your CPF Ordinary Account (OA) can be a powerful tool to help with home loan repayments.

Ways to Use CPF OA for Home Loans:

- Pay for down payments.

- Cover monthly mortgage repayments.

- Pay legal fees and stamp duties.

Important Consideration:

- When you sell the property, you’ll need to refund the CPF principal plus accrued interest (2.5% annually) to your OA.

- This reduces your cash proceeds from the sale.

Important: Remember to account for accrued interest when you sell your property — this amount must be refunded to your CPF. Learn how this affects your overall home loan interest rate in Singapore and plan ahead with the right loan package.

Tools and Tips for Comparing Home Loan Rates

Ready to dive into comparing home loan rates in Singapore? Here are some practical tools and tips to help you make an informed decision—and avoid costly surprises down the line.

Using a Home Loan Calculator to Estimate Payments

Before you sign on the dotted line, plug the numbers into a mortgage loan calculator. It helps you see:

- Your monthly repayment based on loan amount and interest rate.

- How different rates (fixed vs. floating) affect your budget.

- Total interest payable over the loan tenure.

Pro Tip: Use our handy mortgage loan repayment calculator to estimate your payments across different banks and packages.

Reading the Fine Print — Fees, Lock-Ins, and Penalties

Banks love to advertise low rates, but the fine print often hides important details. Watch out for:

- Lock-In Periods: Usually 2-3 years during which early repayment triggers a penalty.

- Early Repayment Penalties: Typically 1.5% of the outstanding loan.

- Valuation and Legal Fees: Some banks subsidize these; others don’t.

Key Fees and Penalties to Check Before Choosing a Home Loan (January 2026)

| Factor | Typical Cost | Notes |

|---|---|---|

| Lock-In Period | 2–3 years | Early repayment incurs a penalty |

| Early Repayment Penalty | 1.5% of loan amount | Check your loan terms |

| Valuation Fees | $200 – $500 | May be subsidised |

| Legal Fees | $1,500 – $3,000 | Some banks offer subsidies |

Expert Tip: Always ask the bank or broker to explain these costs before committing. For more clarity on how these affect your loan, check out our guide to refinancing your home loan in Singapore.

Consulting a Mortgage Broker for Expert Advice

A good mortgage broker can help you navigate the complexities of comparing home loan rates. They:

- Explain the differences between fixed, floating, and hybrid rates.

- Highlight promotions and rebates you might otherwise miss.

- Assist with paperwork and negotiating better deals.

Remember, don’t underestimate the value of having a specialist on your side. Brokers can often spot hidden costs and help you save money in the long run.

Frequently Asked Questions (FAQs)

We get it — comparing home loan rates in Singapore can raise a lot of questions. Here are some of the most common ones our readers ask:

How to Compare Home Loan Rates Without Overpaying?

Start by:

- Comparing rates from at least 3 banks (DBS, UOB, OCBC) side by side.

- Checking lock-in periods, fees, and promotional terms — sometimes a lower headline rate hides higher fees.

- Using a mortgage loan calculator to estimate monthly repayments accurately.

Pro Tip: Even a small difference in interest rate can save you thousands over your loan tenure.

Is It Better to Choose a Fixed or Floating Home Loan Rate?

It depends on your financial goals:

- Fixed Rates: Offer stability in monthly payments — great for budgeting.

- Floating Rates (SORA): Can save you money if rates drop, but payments can also rise.

Personal Opinion: If you prefer predictability, go fixed; if you can handle some risk, floating may save you money. Check out our refinancing guide for more insights.

How Often Do Home Loan Rates Change in Singapore?

- Fixed Rates: Stay the same during the lock-in period (usually 2–3 years).

- Floating Rates: Reviewed every 1–3 months depending on the bank and SORA trends.

Tip: Home loan rates can shift quickly based on market conditions. Stay updated by checking regularly with your preferred bank or trusted mortgage advisor.

Can I Use CPF for My Monthly Mortgage Payments?

Yes! You can use your CPF Ordinary Account (OA) to:

- Pay your monthly mortgage instalments.

- Cover part of your down payment and legal fees.

Important: When selling your home, don’t overlook the CPF refund — you’ll need to return both the principal and accrued interest. Learn more about how CPF affects your HDB home loan here.

How Do TDSR and MSR Affect My Loan Amount?

- TDSR (Total Debt Servicing Ratio): Caps your total monthly debt repayments (including all loans) at 55% of your gross monthly income.

- MSR (Mortgage Servicing Ratio): Applies to HDB flats and ECs, limiting your monthly mortgage repayments to 30% of your gross monthly income.

Pro Tip: Lowering your existing debts can improve your loan eligibility. Use our mortgage loan repayment calculator to plan smarter before applying.

Conclusion: Find the Best Home Loan Rate for You

Finding the right home loan rate in Singapore doesn’t have to be complicated. By understanding how to compare rates, reviewing different loan types, and checking out bank promotions, you can make a decision that saves you money and fits your financial goals.

Remember: even a small difference in interest rate can add up to thousands over the life of your mortgage — so take the time to compare carefully.

Ready to start your homeownership journey? Explore our full range of loan options and expert tips on the Singapore mortgage broker page — your first step to securing the best deal with confidence.