Looking for a home loan in Singapore but feeling a little overwhelmed? You’re not alone. With every bank offering different rates, terms, and “special deals,” it’s easy to get confused.

That’s where a mortgage broker in Singapore comes in. They help you compare across banks, explain the key differences, and make sure you’re not overpaying for your loan.

Whether you’re buying your first flat, upgrading, or planning to refinance your home loan, this guide will show you how a broker can make the process smoother — and help you save time, stress, and money.

Meet the Mortgage Broker: Your Personal Guide to Home Loans in Singapore

Getting a home loan in Singapore isn’t just about finding the lowest rate — it’s about knowing your options. That’s where a mortgage broker comes in. More buyers today are skipping the bank queues and getting expert, bank-neutral advice from professionals who do the comparison work for them.

What exactly is a mortgage broker — and how do they help homebuyers?

A mortgage broker in Singapore acts as your go-between — someone who compares home loan rates, explains all the confusing terms, and helps you secure the best deal based on your needs.

✅ Instead of going bank to bank, a broker:

- Gathers quotes from banks like DBS, UOB, and OCBC

- Helps you understand key terms like lock-in periods, legal subsidies, and floating vs fixed rates

- Advises you on your loan eligibility, CPF usage, and monthly repayments

And yes — their service is usually free. Brokers are paid by the banks, not you.

Expert tip: A good broker won’t just chase the lowest rate. They’ll tailor the recommendation to fit your future plans, whether you’re buying a condo, HDB, or refinancing.

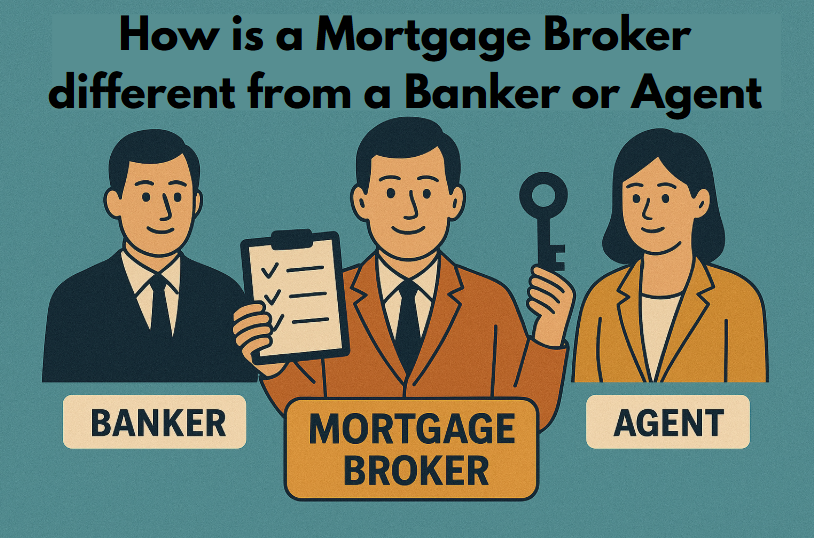

How is a mortgage broker different from a banker or agent?

Many buyers still assume going straight to the bank is the simplest path — but that often means missing out on better options. Here’s a side-by-side view to help you understand the difference.

Mortgage Broker vs Bank Officer in Singapore: Who Offers Better Loan Advice and Options?

| Feature | Mortgage Broker | Bank Officer |

|---|---|---|

| Loan Options | Access to multiple banks and packages | Restricted to their own bank’s products |

| Advice Quality | Neutral, tailored recommendations | Biased towards selling in-house packages |

| Range of Services | Covers HDB, private, refinancing, and commercial property loans | Limited to the bank’s loan offerings |

| Time & Convenience | One-stop comparison across many banks | You must approach each bank individually |

| Payment | Free (brokers are paid by banks) | Free |

A broker is also not a property agent — they don’t push a home to earn commission. Their focus is purely on helping you make a smarter financing decision.

Reference: MAS: Find a Licensed Financial Adviser

Why more Singaporeans are turning to brokers in 2025

As mortgage interest rates in Singapore continue to shift and banks tighten their criteria, buyers are realising it pays to get help.

Whether you’re:

- Buying your first HDB

- Planning to refinance your home loan

- Or comparing rates across banks

A mortgage broker gives you clarity, access, and confidence — without the hard selling.

🧮 Run the numbers first: Use a mortgage loan repayment calculator to preview your monthly costs.

When Should You Use a Mortgage Broker Instead of Going to a Bank?

The short answer? Pretty much anytime you want to be sure you’re getting the best deal — without the headache of comparing rates and policies on your own.

A mortgage broker in Singapore isn’t just for people who are lost or overwhelmed. They’re for anyone who wants to save time, reduce stress, and make confident financial decisions, whether it’s your first HDB or your third private property.

Are brokers helpful for first-time homebuyers?

Yes — especially if you’re feeling unsure where to start.

Brokers can:

- Explain loan types, terms, and repayment options in plain English

- Help you check your HDB loan eligibility and bank loan limits

- Break down how much you can use from CPF, and how to avoid over-borrowing

Most importantly, they help you compare offers across banks — so you don’t end up overpaying simply because you didn’t know there was a better option.

Tip: First-time buyers often underestimate how much bank loan terms can affect long-term affordability. Ask your broker to run your numbers using a home loan calculator before you commit.

What about upgraders or complex loan cases?

Absolutely. If you’re:

- Selling an HDB while buying a condo

- Managing a bridging loan

- Or exploring refinancing your home loan

— a broker is invaluable.

They can time your financing properly, structure CPF refunds smartly, and flag hidden costs like penalty clauses or interest rate resets. That’s something even bank officers may not point out.

Can brokers help even if I already have a bank in mind?

Definitely. Even if you’re leaning toward a DBS home loan, a broker might show you that UOB or OCBC has a better fixed package — or that the refinancing subsidy at another bank offsets the difference entirely.

They can also negotiate on your behalf — sometimes getting better deals than if you walked into the bank yourself.

Pro tip: The best brokers don’t push one bank. They focus on helping you find the right fit — especially if you’re comparing fixed rate home loans in Singapore across several lenders.

How Do Mortgage Brokers in Singapore Make Money?

One of the first things homebuyers ask is: “If the service is free… how do mortgage brokers actually earn?” And it’s a fair question.

Here’s the simple answer: you don’t pay them — the bank does.

Let’s break it down

Is their service really free for buyers?

Yes, 100% free for you.

When you work with a licensed mortgage broker in Singapore, you get all the advice, rate comparisons, paperwork help, and loan planning — without paying anything out of your own pocket.

So how are they paid?

Once you’ve chosen a loan and it’s disbursed, the bank pays the broker a small referral fee. This doesn’t affect your interest rate, loan terms, or approval in any way.

Think of it like this: The bank pays the broker instead of paying a salesperson in a branch. You still get the loan — but with less effort on your part.

Do they earn commission from the banks?

Yes — but here’s why it doesn’t compromise your options.

Most major banks like DBS, UOB, and OCBC offer roughly similar commissions to brokers. That means brokers aren’t financially motivated to push one lender over another.

Instead, they focus on helping you:

- Find the best home loan rates in Singapore

- Avoid hidden fees or lock-in traps

- Choose a package that actually suits your needs

In fact, brokers only get paid if your loan is approved — so it’s in their best interest to recommend a bank that’s likely to say yes and offer a good deal.

💡 Bonus: Some brokers also have access to private promotions or cash rebates that aren’t publicly advertised.

Will I be pressured to choose a certain bank?

If you’re working with a proper, MAS-licensed mortgage advisor — no, never.

A good broker will:

- Show you multiple options side-by-side

- Explain the pros and cons clearly

- Respect your budget and personal preferences

They’re not here to sell you a bank. They’re here to help you choose one confidently.

✅ Trust Tip: Want to double-check if your broker is legit? You can look them up on the MAS directory of licensed financial advisers.

What Types of Loans Can a Mortgage Broker Help You With?

A mortgage broker doesn’t just help you find the lowest rate — they help you choose the right type of loan for your situation.

And no, it’s not just for first-time buyers.

From HDB flats to shophouses, refinancing to business properties, mortgage brokers cover a wide range of loan types — and often spot financing solutions you didn’t know you could access.

Do brokers handle both HDB and private property loans?

Yes — and they’re especially useful when you’re not sure whether to go with a bank loan or an HDB loan.

A broker can:

- Compare HDB loan rates vs bank rates

- Assess your eligibility and MSR/TDSR limits

- Help you decide based on your downpayment, CPF usage, and long-term plans

Whether you’re buying a BTO, resale flat, or looking at private property loans, brokers will lay out all your options — not just what one bank offers.

📌 Explore options: Compare HDB home loan packages or private property loans

Can they assist with refinancing or equity term loans?

Definitely. In fact, refinancing is one of the top reasons people approach brokers.

They can help with:

- Refinancing your HDB loan to get better rates

- Refinancing private property loans after the lock-in period ends

- Structuring equity term loans if you need to unlock cash from your property

Smart move: Many Singaporeans use refinancing to free up funds for renovation, investments, or education — without selling their home.

Are commercial or industrial loans included too?

Yes — experienced brokers also help with:

- Singapore commercial property loans

- Shophouse, warehouse, and office property financing

- Portfolio restructuring for business owners with multiple assets

Commercial loans often have different requirements, interest structures, and risk profiles — so broker support here is especially valuable.

🧠 Pro tip: For business-related properties, brokers can also advise on loan-to-value (LTV) limits, valuation buffers, and exit penalties.

Real-Life Example: How a Broker Helped a Buyer Save $38,000

Not sure if using a mortgage broker in Singapore really makes a difference? Here’s a true-to-life scenario that shows how the right advice at the right time can lead to serious savings.

The buyer’s original situation (tight timeline, two properties, unsure bank approval)

Jason, a 39-year-old homeowner, had just sold his HDB and was upgrading to a condo. But things got messy fast:

- His HDB sale hadn’t completed yet

- He needed to secure a condo quickly before the price went up

- He wasn’t sure which bank would approve his loan while still holding another property

He was also working with a tight timeline and had no idea which home loan in Singapore would give him the flexibility he needed.

What the broker recommended — and how they structured the loan

Instead of jumping straight into the first offer he got, Jason contacted a licensed mortgage broker for advice.

Here’s what they did:

- Ran a detailed comparison of fixed rate vs floating rate packages across 6 banks

- Structured a bridging loan to help cover the overlap between sale and purchase

- Recommended a DBS home loan with a limited-time cashback offer

- Helped him avoid early repayment penalties by matching loan lock-in periods to his plans

Outcome: lower interest rate, faster approval, and avoided penalties

Thanks to the broker’s help, Jason:

- Secured approval in 3 working days (after getting ghosted by his original bank)

- Locked in a better mortgage interest rate than what he was quoted directly

- Avoided $8,000 in potential penalties

- Got $30,000 in interest savings over 5 years

💬 Jason’s takeaway: “I would’ve picked the wrong loan out of panic. The broker made everything clearer — and saved me way more than I expected.”

Want to explore smarter financing options too? Speak to a mortgage advisor before you sign anything.

How to Choose the Right Mortgage Broker in Singapore

Not all mortgage brokers are created equal. While many offer great service, others may be biased, inexperienced, or simply not transparent.

Here’s how to make sure you’re working with someone who truly has your back.

What certifications or licenses should you check for?

Always check that your broker is registered with the Monetary Authority of Singapore (MAS) under the Financial Advisers Act. This ensures they’re legally allowed to provide home loan advice and handle your financial information.

✅ Use the MAS Financial Adviser Directory to verify if the firm is licensed.

Also, ask if they have:

- Relevant certifications or bank accreditation

- At least 2–3 years of experience in Singapore mortgage advisory

- A client-first approach (not just chasing commissions)

Are all brokers MAS-licensed and bank-neutral?

No — and that’s why it matters.

Reputable brokers like those at Ace Mortgage are:

- Bank-neutral (they compare multiple lenders)

- Unbiased (they don’t push one product unless it’s genuinely best for you)

- Updated on market trends, bank promos, and CPF usage policies

Avoid anyone who:

- Offers just one bank’s loan

- Doesn’t explain other options

- Refuses to show you side-by-side comparisons

🧠 Smart tip: Ask how many banks they work with. A strong broker panel usually includes DBS, UOB, OCBC, and more.

Red flags: When to walk away from a broker

Keep an eye out for these warning signs:

❌ Only showing one bank’s package

❌ Avoids your questions or rushes you to sign

❌ Charges you a “consultation fee” upfront

❌ Makes vague claims without showing clear comparisons

❌ Doesn’t provide a written breakdown of loan scenarios

You deserve clarity — not pressure.

🔍 Pro tip: If something feels off, it probably is. A reliable broker is open, thorough, and always willing to explain how they earn and what’s in it for you.

Benefits of Using a Singapore Mortgage Broker

If you’re wondering whether it’s worth speaking to a mortgage broker, here’s what you actually get — beyond just rate comparisons.

A good mortgage broker in Singapore gives you clarity, speed, and access to deals you probably won’t find on your own.

Access to exclusive rates and cashback deals

Brokers often work directly with bank reps and get early access to:

- Limited-time cash rebates, subsidised legal fees, and valuation waivers

- Promo-only fixed rate home loans not listed online

- Special offers for refinancing or private property loans

Banks may not advertise these deals openly — but brokers know when they’re available and who qualifies.

🔍 Compare the latest DBS, UOB, and OCBC home loan offers through a single broker platform.

Transparent advice tailored to your situation

Unlike bank officers who are tied to one lender, brokers look at:

- Your income structure, age, CPF balance, and financial goals

- Whether you plan to sell, refinance, or invest in future

- Loan types that actually fit your risk appetite and timeline

No pushy sales. Just smart, personalised advice to help you make the right call.

💬 “My broker told me not to go with the lowest rate — and he was right. The package he recommended saved me $12k in lock-in penalties.” — Actual client via Ace Mortgage

Simplified loan comparisons across multiple banks

Trying to compare home loan rates across banks is a pain — especially when each uses different terms, formats, and lock-in clauses.

A broker:

- Organises all your options side-by-side

- Highlights key differences clearly

- Flags red flags like clawbacks, repricing limits, or CPF restrictions

All in one place, without hours of Googling.

✅ Save time and energy by using a mortgage loan repayment calculator to see how each loan stacks up.

Common Misconceptions About Mortgage Brokers

Still on the fence about using a broker? You’re not alone.

Here are some of the biggest myths — and the real truth behind them.

Do brokers only work with certain banks?

Nope.

A good mortgage broker in Singapore works with a panel of all major banks — including DBS, UOB, OCBC, and more.

They’re bank-neutral, which means they don’t push one product just because it earns more commission. Most banks pay similar fees anyway — so brokers are more focused on helping you get approved and stay happy.

💡 Tip: Ask your broker how many banks they work with. More banks = more choices = better odds of landing the ideal loan.

Is it better to go directly to the bank instead?

Only if you enjoy doing all the work yourself 😅

Going direct means:

- You’ll only see that bank’s products

- You’ll have to repeat your financial info again and again

- You may miss out on better rates or cashback elsewhere

Using a broker means:

- One point of contact

- Full access to multiple banks

- Professional help comparing and applying

✅ Best part? It still costs you nothing. You get more options — with less stress.

Are online platforms the same as human brokers?

Not quite.

Comparison platforms are great for basic rate checks. But they don’t:

- Analyse your situation in depth

- Flag things like loan eligibility issues or CPF usage limits

- Negotiate directly with bank reps on your behalf

A real broker offers human advice, context, and long-term strategy — especially helpful when you’re refinancing, buying your second property, or managing multiple loans.

🤝 Combine the best of both: use platforms for browsing, but speak to a licensed broker for real clarity.

Frequently Asked Questions About Mortgage Brokers

Still got questions? Totally normal.

Here are some common concerns homebuyers (and even upgraders) have when considering a mortgage broker in Singapore.

Can foreigners or PRs use mortgage brokers?

Yes — absolutely.

Whether you’re a Singapore PR or a foreigner, mortgage brokers can help you:

- Understand loan eligibility rules for non-citizens

- Compare banks that offer loans to PRs and foreigners

- Navigate loan-to-value (LTV) limits and income requirements

Some banks are stricter with foreigners or require higher downpayments — but a broker will help you filter quickly and avoid wasting time.

🧭 Planning to buy in Singapore as a non-citizen? A broker can guide you through the process before you even start viewing properties.

How early should I speak to one during my property journey?

The earlier, the better.

You don’t need to wait until you’ve picked a flat or condo. In fact, it’s ideal to speak to a broker when:

- You’re starting to research your options

- You want to know your home loan eligibility

- You’re trying to set a budget based on monthly repayments

📈 Early advice helps you avoid overcommitting — and gives you confidence during viewings and negotiations.

Try this: Use a mortgage loan calculator first, then speak to a broker to plan the next step.

Will using a broker affect my credit score?

Nope. Not at all.

Brokers do not run credit checks themselves. They only collect your documents and submit them to your chosen bank after you decide to proceed.

Only the bank runs the actual credit assessment — and even then, a single check has minimal impact (unless you’re applying to many banks at once).

✅ Good to know: Your credit score is safe while you’re comparing — so don’t be afraid to explore your options with a broker first.

Speak to a Trusted Mortgage Broker in Singapore Today

When it comes to choosing a home loan in Singapore, timing isn’t just important — it’s everything.

Whether you’re weeks away from booking a unit or still figuring out your budget, speaking to a mortgage broker early can save you from costly mistakes later.

Why timing matters — pre-approval vs post-purchase regret

Getting pre-approved helps you:

- Know exactly how much you can borrow

- Avoid delays when booking or exercising your Option

- Negotiate better with sellers or agents

Too many buyers wait until it’s almost too late — then rush into a loan without knowing if it’s the best fit. That’s when regret kicks in.

What to expect during your free consultation

It’s zero-pressure, completely free, and 100% personalised.

A licensed broker will:

- Understand your needs, timeline, and financial situation

- Compare the latest home loan rates in Singapore

- Recommend the best packages — including hidden perks like cashback, fee waivers, or legal subsidies

You’ll walk away with clarity, not confusion.

Compare DBS, OCBC, UOB and more — with zero bias

Whether you’re considering a DBS home loan, OCBC mortgage, or UOB refinance package, a broker will lay out everything side by side — clearly and objectively.

No hard sell. No guesswork. Just smart, data-driven advice tailored to you.

Final Thoughts — Why a Mortgage Broker Could Be Your Smartest Move

Finding the right home loan in Singapore isn’t just about chasing the lowest interest rate — it’s about knowing what fits your life, your finances, and your future plans.

A trusted mortgage broker helps you cut through the noise, compare bank options with zero bias, and avoid costly surprises — all without charging you a fee.

Whether you’re a first-time buyer, looking to refinance your HDB loan, or upgrading to private property, speaking to a broker early can save you time, money, and stress.

Ready to make a confident move?

Speak to a Singapore mortgage broker for free today.

No pressure — just real, personalised advice to help you choose the right loan.