Thinking about renting out a property in Singapore? Before you count on that passive income, it’s crucial to understand what you’re really paying for. From stamp duties to monthly loan repayments, MCST fees to vacancy costs—these add up fast.

In this guide, we break down the total cost of owning a rental property in Singapore. Whether it’s a HDB unit or private condo, we’ll show you how to budget smart, spot hidden fees, and protect your ROI.

Let’s get into it.

Upfront Costs When Buying a Rental Property

It’s tempting to focus only on the purchase price—but in reality, your initial cash outlay includes several other big-ticket items. Whether you’re eyeing a private condo or planning to rent out your HDB flat after MOP, understanding the true upfront costs is key to protecting your rental yield.

Buyer’s Stamp Duty (BSD), Legal Fees & Valuation Costs

Buyer’s Stamp Duty (BSD) is the first major cost you’ll encounter, and it can quickly climb into the five-digit range. For example, a $1 million property could incur $24,600 in BSD alone.

To get an estimate for your property, try this BSD calculator or check IRAS’s official stamp duty breakdown.

Other essential costs include:

- Conveyancing/legal fees: Usually ~$2,500 to $3,500 depending on whether you use a bank panel lawyer.

- Valuation report: Required for bank loans, and typically ranges from $300–$500.

Expert Tip: If you’re using a mortgage broker in Singapore, they’ll often advise you on legal panel choices that can save you hundreds.

Renovation, Furnishing & Home Staging Budget

If you want to attract good tenants—and command higher rent—be prepared to spend on renovations and furnishings. Here’s a rough guide:

Estimated Renovation and Furnishing Costs for Rental Property in Singapore

| Item | Estimated Budget Range (SGD) |

|---|---|

| Light renovation (painting, fixtures) | $10,000–$20,000 |

| Full renovation (kitchen, bathroom) | $30,000–$50,000+ |

| Furniture and electrical appliances | $5,000–$10,000 |

| Optional home staging for rental unit | $1,000–$3,000 |

Units that are well-renovated and move-in ready often fetch 10–15% more in monthly rent—especially in the condo market.

Option Fees, Booking Fees & Misc Charges

Smaller fees add up too. Don’t forget:

- Option Fee: Usually 1% of the purchase price.

- Exercise Fee: 4% upon exercising the Option to Purchase (OTP).

- Admin/Misc Charges: $200–$500 for things like caveat lodgement or CPF legal paperwork.

While they may seem minor, these can still total a few thousand dollars—and should be included in your cost of buying rental property in Singapore.

Monthly and Recurring Ownership Costs

Owning a rental property in Singapore isn’t just about the one-time fees upfront — it’s the recurring monthly costs that can eat into your rental income if you’re not careful. These costs affect your net rental yield and ROI, so it’s essential to track them closely, especially if you’re financing through a home loan in Singapore.

Let’s break it down.

Monthly Loan Repayments (Bank vs HDB Loan)

If you’re using a bank loan or HDB loan, your biggest monthly expense will likely be your mortgage repayment.

- For HDB loans (2.6% interest rate), repayments tend to be more stable — but limited to HDB flats only.

- For bank loans, you may get a lower rate initially, especially if you’re comparing options like DBS home loan,UOB home loan, or OCBC home loan.

Use a mortgage loan repayment calculator to estimate your monthly repayments based on tenure, loan amount, and interest rate.

Pro Tip: Even a 0.5% difference in mortgage interest rate in Singapore can shift your ROI by a few thousand dollars a year — don’t set and forget.

Property Tax, Condo MCST Fees, and Insurance

Beyond the loan, you’ll need to factor in:

- Property tax: Based on the Annual Value (AV) of your unit. Higher AV = higher tax, especially for non-owner-occupied units.

- MCST fees (condo maintenance): Typically $250–$400/month, depending on unit size and condo facilities.

- Landlord insurance: Optional but smart. Covers fire damage, loss of rent, and liability — usually around $200–$300/year.

All these are part of your rental property ownership cost in Singapore, and they directly reduce your net rental yield.

Accounting, Agent Commissions & Other Holding Costs

Other ongoing costs include:

- Rental agent commissions: 1-month rent for a 2-year lease (paid once every two years).

- Bookkeeping/tax filing: If you’re declaring rental income, you may want a professional to help with IRAS submissions.

- Ad hoc repairs: Set aside 1–2 months of rent annually for things like plumbing, aircon servicing, or appliance replacement.

Keeping a buffer for these will help you avoid surprises and maintain positive rental cash flow.

Hidden Costs That Landlords Often Miss

Even seasoned landlords in Singapore sometimes overlook the “silent killers” of rental ROI. These hidden rental property costs may not show up in your initial budget — but they definitely show up in your returns. If you want to get an accurate picture of your net rental yield in Singapore, you need to account for these too.

Let’s go through the most common ones.

Vacancy Periods, Tenant Turnover & Agent Commissions

Vacancies happen — even in high-demand areas. You might have a 1–2 month gap between tenants, and that’s 100% income loss for those months.

- Tenant turnover means repainting, minor repairs, and marketing costs.

- Agent commissions typically cost 1 month’s rent for a 2-year lease, or more for shorter leases or repeat placements.

Expert Tip: Always buffer for at least 1 month of vacancy per year in your ROI calculations. For condos in popular districts, the rental gap may be shorter — but it’s still a risk.

Unexpected Maintenance, Repairs & Furniture Replacement

That new aircon? It won’t stay new for long. Here’s what often surprises landlords:

- Aircon servicing every quarter (~$120/year)

- Water heater or washing machine replacement (~$300–$800)

- Repainting, plumbing, or fixture replacements between tenancies

While these seem minor, they add up quickly and can quietly chip away at your profit. Many investors in Singapore forget to factor in a “sinking fund” of at least 5–10% of annual rent.

Mortgage Repricing or Early Repayment Penalties

Bank loans in Singapore often come with lock-in periods. If you refinance or repay early, watch for:

- Repricing fees (typically $500–$1,000)

- Penalty interest or clawbacks if you switch banks too soon

- Legal and valuation costs if refinancing mid-loan

Check your loan agreement carefully — especially if you’re on a fixed package from DBS, OCBC, or UOB.

You can also use a mortgage broker in Singapore to help you navigate this and avoid unnecessary costs.

What Affects the Total Cost Most

When calculating the total cost of owning a rental property in Singapore, it’s not just about the purchase price. Ongoing factors like loan terms, property type, and even location-specific fees can cause huge variations in your real ROI.

Let’s break down the biggest cost influencers for landlords.

Interest Rates, Loan Tenure & Repricing Strategy

Your monthly mortgage repayment depends heavily on your loan tenure and whether you’re on a fixed or floating interest rate.

- A shorter tenure = higher monthly cost, but less total interest paid.

- A longer tenure = lower monthly cost, but higher long-term interest.

Home loan rates in Singapore can range from 1.3–3.5% p.a. depending on the bank and package. But repricing at the right time can significantly reduce costs.

Expert Tip: Always compare between DBS, OCBC, and UOB using a mortgage broker in Singapore to get better rates and cashback offers.

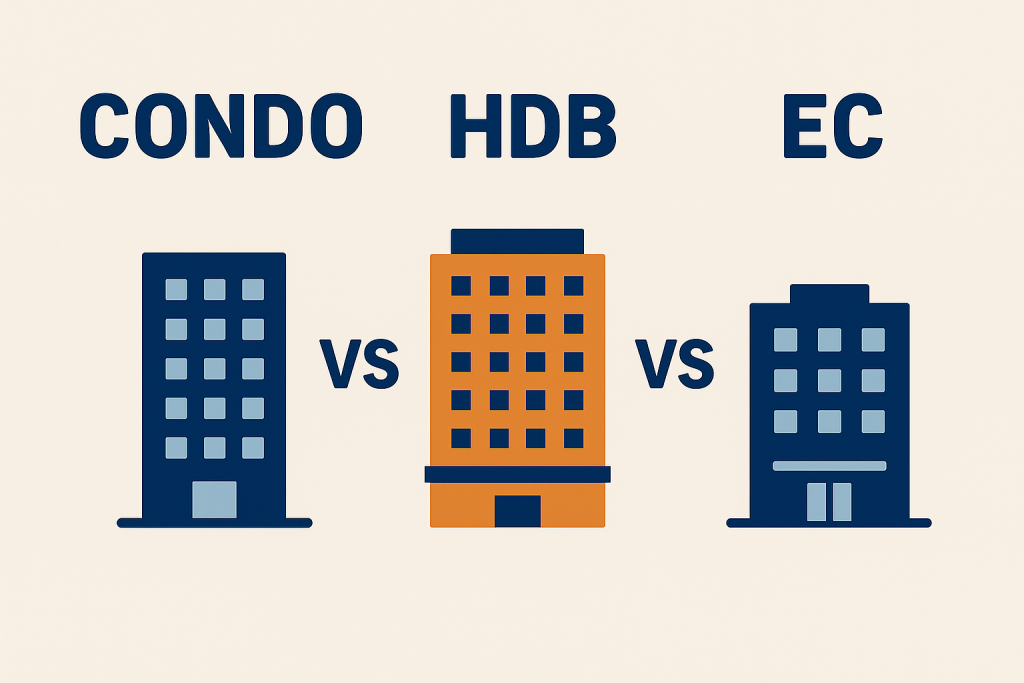

Type of Property: Condo vs HDB vs EC

Each property type carries different cost burdens:

Cost Comparison by Property Type in Singapore for Rental Investment

| Property Type | Typical Loan Type | Additional Ownership Costs |

|---|---|---|

| HDB Flat | HDB Loan / Bank Loan | Lower property tax, no condo MCST fees |

| Executive Condo | Bank Loan only | Property tax, partial MCST after MOP |

| Private Condo | Bank Loan only | MCST fees, higher renovation and furnishing costs |

Location-Based Factors: MCST Fees, Rental Demand

Where your unit is located impacts:

- MCST (maintenance) fees — $250 to $500/month for condos, depending on facilities.

- Rental demand — higher in central regions (e.g. D9, D10), but so are prices and competition.

- Property tax — based on annual value (AV), which is influenced by the location’s rent potential.

📍 For example, a 2-bedder in District 15 (East Coast) may have stronger expat appeal, but higher MCST fees than a comparable unit in the OCR.

If you’re buying for yield, weigh rental demand vs ownership cost before committing.

How to Optimise Costs Without Sacrificing ROI

Not all cost-cutting is smart — especially when it comes to rental properties. The goal isn’t just to save money, but to spend it strategically to maximise your rental yield in Singapore. Here’s how savvy investors keep their expenses lean without hurting long-term returns.

Choosing Low-Maintenance Units or Dual-Key Layouts

Units that are easy to maintain can save you thousands in upkeep over the years. Think:

- Newer condos with still-valid warranties

- Smaller units = less to clean, less to break

- No high-maintenance flooring or fragile built-ins

Dual-key layouts are another ROI hack. They let you rent out two spaces separately, potentially earning 20–30% more while sharing one mortgage.

Pro Tip: Units near MRTs with efficient 2BR or dual-key layouts tend to offer the best balance of cost and rental demand.

When to Renovate vs When to Leave As-Is

Not every unit needs a full makeover. Sometimes, basic touch-ups (paint, lighting, cabinet polish) are enough to attract solid tenants. You want to renovate only if:

- The rent you can command justifies the renovation spend

- It gives you an edge in a highly competitive location

- The ROI on renovation is recoverable within 12–18 months

Otherwise, you’re just sinking cost into vanity upgrades.

Using a Mortgage Broker to Compare Bank Packages

Many property investors lose money simply by choosing the wrong home loan.

Mortgage rates in Singapore can vary greatly — from fixed packages with higher upfront costs to floating rates that may spike unexpectedly. That’s where a mortgage broker in Singapore comes in.

They’ll help you:

- Compare DBS vs UOB vs OCBC packages side by side

- Understand hidden costs like repricing fees or clawbacks

- Pick a loan that fits your investment timeline and budget

Want a shortcut? Try our mortgage loan repayment calculator to estimate your monthly outlay before you commit.

Final Thoughts – Know the Real Cost Before You Buy

Buying a rental property in Singapore isn’t just about the purchase price — it’s about understanding the true long-term cost of ownership. From monthly loan repayments and property tax to vacancy risk and maintenance, the smartest landlords plan for every cent.

Whether you’re a first-time investor or scaling your property portfolio, take the time to break down the numbers, weigh your options, and get advice before signing anything.

Link to Mini Article: How to Calculate Rental Yield

Not sure if your investment is worth it? Check out our full guide:

→ How to Calculate Rental Yield Like a Pro (Singapore Edition)

We break down gross vs net yield, rental benchmarks, and what’s considered a “good” yield in today’s market.

Link to Case Study: Singapore Rental Property ROI

Want a real-life example?

→ Case Study: How One Buyer Turned a 2-Bedder into a 4.5% Yield Rental in 2025

Learn what worked, what didn’t, and how cost planning made all the difference.

Speak to an Advisor to Plan Based on Your Budget

Don’t guess your numbers — plan them.

A licensed mortgage advisor in Singapore can walk you through the best loan packages, help you avoid costly mistakes, and map out a plan based on your budget, property type, and rental goals.

Tip: Whether you’re eyeing a UOB home loan,OCBC home loan, or refinancing options, expert advice could save you thousands in the long run