Looking to understand loan principal and bank interest rates in Singapore this year? You’re not alone! With so many banks and packages out there, it can be overwhelming — but it doesn’t have to be.

In this guide, I’ll break down what loan principal really means, how it affects your monthly payments, and why understanding your interest rates — especially with the latest SORA benchmarks — can help you save.

Whether you’re a first-time buyer, refinancing, or just exploring your options, this guide will give you the clarity and confidence to make smarter decisions. Let’s dive in! And don’t forget to visit our Ace Mortgage homepage for the latest tools and expert tips.

What is Loan Principal and Why It Matters?

When you’re planning to buy a home in Singapore, understanding the loan principal is crucial. It’s the foundation of your mortgage — the amount you actually borrow to pay for your property. But that’s just the beginning.

Knowing how it interacts with interest rates and the Loan-to-Value (LTV) ratio can make a big difference in how much you pay over the life of your loan. Let’s break it down so you can make smarter decisions with confidence.

Understanding Loan Principal vs. Interest

Loan Principal:

- The core amount you borrow from the bank to buy your home.

- Directly goes toward the property price.

Interest:

- The cost of borrowing, charged by the bank.

- Calculated as a percentage of your outstanding principal.

Expert Tip: Keep an eye on how much of your monthly repayment goes toward principal vs. interest — it can affect how fast you pay off your loan.

Use our home loan calculators to estimate your payments and see how different rates affect your budget.

How Loan-to-Value (LTV) Impacts Your Principal Amount

Your Loan-to-Value (LTV) ratio determines how much of a property’s value you can borrow — and it directly affects your loan principal.

In Singapore, your LTV depends on whether you’re buying your first home or already have an existing mortgage. Here’s a quick look at the current LTV limits in 2025:

Maximum LTV Ratios and Principal Loan Amounts in Singapore (2025)

| Buyer Type | Max LTV (2025) | Principal You Can Borrow |

|---|---|---|

| First-Time Buyer | Up to 75% | Higher principal amount |

| Second Mortgage | Up to 55% | Lower principal amount |

- The higher your LTV, the more you can borrow — but remember, this means higher monthly payments too.

- A lower LTV means a smaller principal loan and less interest paid overall.

A higher down payment reduces your principal loan and saves you money in the long run.

Strategies to Reduce Your Principal Faster

Want to pay off your mortgage sooner and save on interest? Here’s how:

- Make extra payments: Top-up your monthly payments or make lump-sum payments whenever possible.

- Shorten your loan tenure: A 20-year loan means less interest than a 30-year one — even if monthly payments are higher.

- Consider refinancing: Switch to a lower interest rate package when market conditions are favorable.

Using part of your bonus or tax refund for extra payments can make a big difference over time. Don’t forget to explore our refinancing page for the latest offers and expert tips.

Exploring Bank Interest Rates in Singapore (2025)

Interest rates are one of the biggest factors affecting your home loan in Singapore. From fixed rates that provide stability to floating rates that adjust based on the market, it’s important to understand how they work — and what to expect in 2025.

Let’s break it down so you can make a smart decision for your property financing.

Fixed vs. Floating Interest Rates — What’s the Difference?

When it comes to choosing your home loan package, banks typically offer two main types:

Fixed Rates:

- Stay the same during the lock-in period (usually 2-3 years).

- Provide stability — perfect if you prefer predictable payments.

- Rates for 2025 are currently around 2.10% to 2.50%.

Floating Rates:

- Adjust periodically (monthly or quarterly) based on market benchmarks like SORA.

- Rates can rise or fall — great if you’re comfortable with some risk and potential savings.

- As of June 2025, floating rates average 2.1931% to 2.2692%.

Expert Tip: Consider your financial goals and risk appetite before deciding. Learn more in our fixed vs. floating rate guide for a deeper dive.

SORA Benchmark Rates — What You Need to Know

If you’re considering a floating interest rate home loan in Singapore, you’ll need to understand how SORA (Singapore Overnight Rate Average) works.

SORA is now the main benchmark banks use to determine your loan rate — and choosing between 1-month vs. 3-month SORA can impact how your repayments fluctuate. Here’s the latest update for June 2025:

Latest SORA Benchmark Rates in Singapore (January 2026)

| Benchmark | Average Rate (November 2025) |

|---|---|

| 1-Month SORA | 1.14% |

| 3-Month SORA | 1.24% |

- SORA (Singapore Overnight Rate Average) is the main benchmark for floating home loans.

- The 1-month SORA typically offers more frequent adjustments, while the 3-month SORA provides more stability.

Pro Tip: Check the MAS official SORA rates regularly for the latest updates. For a quick breakdown, see our SORA guide and compare rates across banks.

Forecasting Interest Rate Trends for 2025

Wondering where interest rates are headed this year? Here’s what the experts are saying:

- Rate Cuts Possible: Analysts predict potential rate cuts in the second half of 2025 if inflation stabilizes.

- SORA Trends: Expected to hover between 2.1% and 2.5% — still lower than pre-pandemic peaks.

- Fixed Rate Packages: Banks may offer promotional rates below 2.5% to attract new customers.

Personal Insight: If you’re considering refinancing, this might be a great window to secure a better rate. Check out our refinancing guide for the latest offers and tips.

How Loan Principal and Interest Rates Impact Loan Approval

When you’re applying for a home loan in Singapore, it’s not just about choosing the best rate or the highest principal — it’s about how these factors impact your overall eligibility. Banks look at your loan principal, interest rates, and financial health to decide how much they’ll lend you.

Let’s unpack how this all comes together so you can plan wisely and improve your chances of approval.

How Loan Principal Influences Borrowing Power

The loan principal plays a huge role in determining how much you can actually borrow. Here’s why:

- Higher Principal = Higher Monthly Payments: The bigger the loan, the more you pay each month.

- TDSR Limit (55%): Banks in Singapore use the Total Debt Servicing Ratio (TDSR) to ensure your monthly repayments (including your new loan) don’t exceed 55% of your gross monthly income.

- Income Requirements: Higher loan principal means higher income requirements to meet TDSR thresholds.

Expert Tip: Use our home loan calculator to see how your loan principal affects monthly payments and eligibility.

How Interest Rates Affect Monthly Repayments

Interest rates are a key factor in your monthly payments. Here’s how:

- Higher Rates = Higher Monthly Repayments: Even a 0.5% difference can mean hundreds of dollars each month.

- Fixed vs. Floating: Choose wisely — fixed rates provide stability, while floating rates (like SORA) can fluctuate.

(Based on $500,000 loan principal, 25-year tenure)

Example: Monthly Repayment Estimates

| Interest Rate | Estimated Monthly Payment |

|---|---|

| 2.1% | ~$2,150 |

| 2.5% | ~$2,240 |

| 3.0% | ~$2,370 |

Personal Insight: Shopping around for the best rate can save you thousands over the life of your loan. Check out our Singapore mortgage rate comparison to see which banks are offering the most competitive rates today.

How Banks Assess Applications Based on Principal and Rates

Banks consider several factors when evaluating your loan application:

- Principal vs. Income: They assess if your income can support the requested principal amount while staying within the 55% TDSR limit.

- Interest Rates: Higher interest rates can reduce your borrowing power because of higher monthly repayments.

- Credit Score: A good credit history boosts your chances of approval, even if your principal is on the higher side.

Expert Tip: Keep your credit score healthy and minimize other debts to maximize your borrowing potential. Learn more about TDSR and how it affects your loan eligibility in our TDSR guide.

Managing Principal and Interest During Loan Repayment

Once your home loan is approved, it’s important to understand how your repayments actually work. Managing your loan principal and interest payments wisely can help you save money and even pay off your mortgage faster.

Let’s look at how it all comes together — from amortization schedules to extra repayments and refinancing options.

Understanding Amortization Schedules

An amortization schedule shows how your loan balance is repaid over time, splitting each payment into principal and interest. Here’s what you need to know:

- Early Years: Payments are mostly interest, with a small portion going towards principal.

- Later Years: More of each payment goes towards reducing your principal.

(Based on $500,000 loan, 25 years, 2.5% rate)

Example: Amortization Snapshot

| Year | Interest Paid | Principal Paid |

|---|---|---|

| Year 1 | $12,350 | $7,600 |

| Year 5 | $11,300 | $8,600 |

| Year 10 | $9,500 | $10,400 |

Expert Tip: Understanding your amortization schedule helps you plan extra payments more effectively. Use our loan repayment calculator to see how your repayments are structured.

Making Extra Repayments — When and Why

Want to pay off your mortgage faster and save on interest? Here’s how:

- Annual Bonuses: Use part of your bonus to pay a lump sum toward your principal.

- Regular Top-Ups: Even small extra payments each month can shorten your loan term.

- Prepayment Options: Check with your bank for any penalties or fees before making extra payments.

I always recommend clients set aside a small percentage of their salary for ad-hoc principal repayments. It’s a simple habit that can cut years off your loan.

Learn more in our refinancing page — sometimes, a new package can allow for easier extra payments!

Refinancing Options to Lower Interest Rates

Refinancing can be a smart move, especially if interest rates have dropped since you took out your original loan. Here’s what to consider:

- Current Market Rates: In 2025, fixed rates average 2.10%–2.50% and SORA-based rates hover around 2.1931%–2.2692% — often lower than older packages.

- Lock-In Periods: Watch out for penalties if you refinance during your lock-in.

- Cost-Benefit Analysis: Factor in legal fees and subsidies when calculating potential savings.

Pro Tip: Use our refinance calculator to see how much you could save. Or check out our latest refinancing offers for the best rates in Singapore.

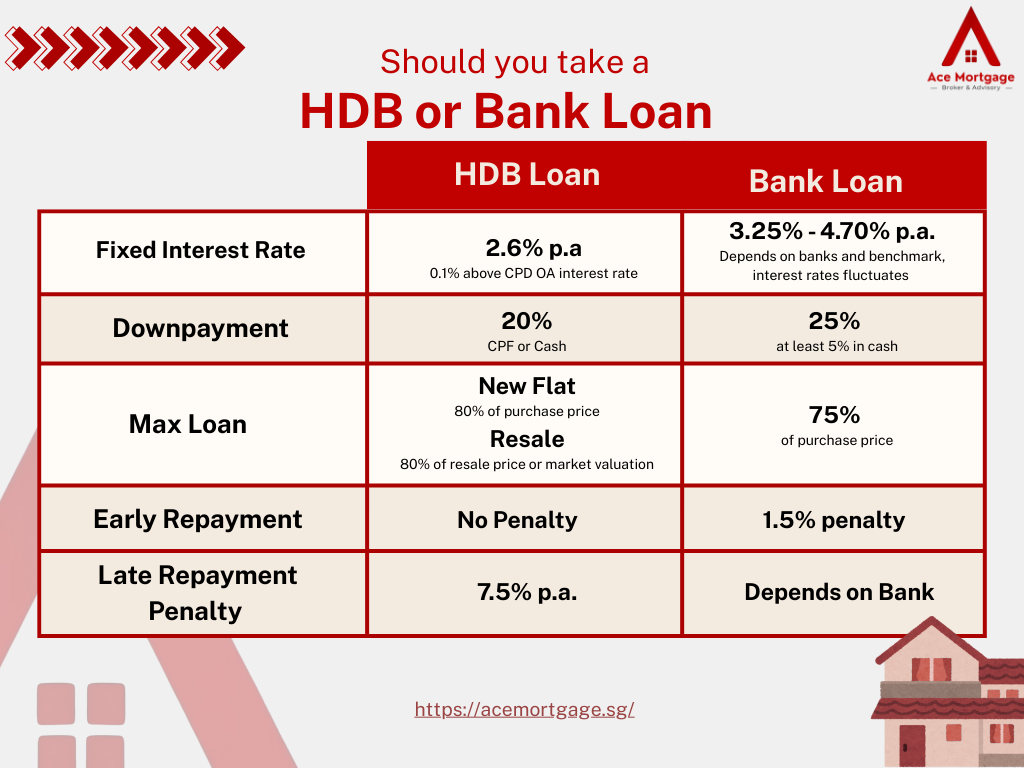

Comparing Bank Loans vs. HDB Loans in Singapore

Choosing between a bank loan and an HDB loan is one of the biggest decisions you’ll make as a homeowner in Singapore. Each has its pros and cons — from interest rates to repayment flexibility.

Let’s dive into how they compare in 2025 so you can pick the one that best suits your needs.

Interest Rate Comparison — June 2025 Update

Interest rates are often the first thing buyers compare when deciding between a bank loan and an HDB loan.

Home Loan Interest Rates in (January 2026)

| Loan Type | Interest Rate |

|---|---|

| HDB Loan | 2.60% (fixed) |

| Bank Loan | ~1.48%–2.75% (fixed) ~1.39%–2.42% (SORA-based) |

- HDB Loan: Pegged at 0.1% above CPF OA interest rate (currently stable at 2.60%).

- Bank Loans: Offer both fixed and floating options, often lower than HDB but can vary over time.

Expert Tip: Compare rates across banks before deciding. Use our latest mortgage rates guide to find the most competitive offers in Singapore.

Flexibility, Lock-in Periods, and Early Repayment

Besides interest rates, consider how flexible each loan type is:

HDB Loans:

- No lock-in period — you can switch to a bank loan anytime.

- More stable, especially helpful if you prefer consistent payments.

Bank Loans:

- Usually come with a 2-3 year lock-in period — early repayment during this time may incur penalties.

- Offer options to reprice or refinance for potentially better rates.

Personal Insight: If flexibility is a priority, an HDB loan might suit you better initially — but bank loans often offer lower rates. Check out our refinancing guide to explore switching options after your lock-in ends.

Which Loan is Right for You?

The best loan for you depends on your financial goals, risk appetite, and lifestyle. Here’s a quick breakdown:

- HDB Loan:

- Great for first-time buyers who value stability and easier eligibility.

- Allows for CPF usage with less stringent credit checks.

- Great for first-time buyers who value stability and easier eligibility.

- Bank Loan:

- Suitable for those who want potentially lower rates and are comfortable with rate fluctuations.

- Better for buyers planning to sell or refinance after a few years.

- Suitable for those who want potentially lower rates and are comfortable with rate fluctuations.

Pro Tip: Talk to a mortgage advisor to assess your options. Our team at Ace Mortgage can help you compare packages and find the best fit for your needs.

Hidden Costs and Features to Watch Out For

When comparing home loans in Singapore, don’t just focus on the headline interest rates. There are hidden costs and features that can surprise you if you’re not prepared. Let’s break down the key details to look out for — so you can avoid unwelcome surprises later on.

Rate Caps, Floors, and Hidden Clauses

Especially with floating-rate loans tied to SORA, banks often set rate caps and floors to protect themselves from market swings. Here’s what to watch for:

- Rate Caps: The maximum rate your loan can hit — for example, a cap of 3.5%.

- Rate Floors: The minimum rate charged even if SORA falls — sometimes 1.5% or higher.

- Hidden Clauses: Watch out for administrative fees, compulsory fire insurance, or valuation costs buried in the fine print.

Expert Tip: Always read the terms carefully. Ask your mortgage advisor to clarify rate caps and floors before signing.

Prepayment Penalties and Waivers

Paying off your loan early sounds great — but some banks charge prepayment penalties during the lock-in period. Here’s what you need to know:

- Penalty Fees: Usually range from 1.5% to 2% of your outstanding loan.

- Partial Repayment Limits: Some banks cap how much extra you can repay per year.

- Waivers: Some lenders waive penalties if you sell your home — but conditions apply.

I’ve seen clients get caught off guard by these fees. Always check your bank’s policy or get help from a mortgage advisor. Our mortgage broker service connects you with experts who can guide you through the fine print and help you avoid costly surprises.

The Role of Mortgage Insurance

Mortgage insurance is often required — but many borrowers don’t realize how it works:

- HDB Loans: HDB requires the CPF Home Protection Scheme (HPS).

- Bank Loans: You may need a private mortgage insurance policy.

- Purpose: Pays off your loan if something happens to you — giving your family peace of mind.

Pro Tip: Don’t assume all insurance policies are the same. Check coverage, exclusions, and compare rates. For guidance, visit our mortgage insurance insights to get the full picture.

Conclusion: Making Informed Decisions for Your Singapore Home Loan

Choosing the right home loan in Singapore doesn’t have to be overwhelming. By understanding your loan principal, interest rates, and all the hidden costs involved, you’re well on your way to making a smarter, more confident decision.

Remember:

- Compare fixed vs. floating rates to find the best fit for your budget.

- Factor in the Loan-to-Value (LTV) ratio and amortization schedules to understand your payments over time.

- Look out for rate caps, floors, and prepayment penalties to avoid surprises later.

And don’t forget to review mortgage insurance requirements for your peace of mind.

Ready to get started? Find out the best mortgage rates here to explore Singapore’s best home loan rates, calculators, and expert advice. Let’s make your property journey smooth, affordable, and stress-free!