The Prime Location Public Housing (PLH) model in Singapore has reshaped the way homebuyers approach living in coveted city areas. Designed to keep housing affordable in prime districts while ensuring fair allocation, the PLH model introduces new eligibility criteria, resale restrictions, and a longer Minimum Occupation Period (MOP).

In this guide, we’ll dive into everything you need to know about the PLH model — from its key features to its implications on resale and upgrading. Plus, we’ll compare it to other housing models and share expert tips on navigating the Singapore property market.

Stay ahead in your homebuying journey with the latest updates, expert insights, and a clear roadmap to understand the PLH model in 2025.

What Is the PLH Model and Why Was It Introduced?

The Prime Location Public Housing (PLH) model is Singapore’s solution to managing demand and prices in prime areas like the city centre and the Greater Southern Waterfront. Introduced in late 2021, it aims to keep these highly coveted flats affordable for Singaporeans while ensuring fair access.

Addressing the ‘Lottery Effect’ in Prime HDB Locations

In sought-after estates like Pinnacle@Duxton, owners have enjoyed windfall profits from high resale values — known as the “lottery effect.”

The PLH model curbs this by introducing a 10-year Minimum Occupation Period (MOP) — double the standard 5 years — to promote owner-occupation and reduce speculative sales.

| Key Feature | Details |

|---|---|

| Lottery Effect | Mitigated by longer MOP |

| MOP Duration | 10 years (vs. 5 years for standard HDB) |

| Target | Prime areas with high resale demand |

I would say consider the commitment of a 10-year MOP before buying. It’s a lifestyle investment, not a quick profit.

Ensuring Long-Term Affordability in Central Areas

The PLH model includes additional subsidies on top of existing grants, helping more Singaporeans buy homes in prime areas. However, these subsidies come with subsidy recovery upon resale, ensuring that future buyers can also access affordable housing.

Key Points:

- Extra subsidies help lower upfront costs.

- Subsidy recovery maintains fairness for future buyers.

- Affordability is a key focus for prime HDB estates.

Check out Ace Mortgage for up-to-date home loan rates and financing tips in Singapore’s competitive property market.

Promoting Inclusive Communities in Prime Locations

The government designed the PLH model to foster inclusive and diverse communities, avoiding pockets of exclusivity in prime areas. By prioritizing Singaporean families and restricting speculative buying, the PLH model supports balanced and vibrant neighbourhoods.

- Singaporean families are prioritized.

- Owner-occupier requirement helps community-building.

- Restrictions on renting the whole flat preserve long-term residence.

Building a home in a PLH flat means investing not just in property but in your future community. Stronger ties, more neighbourly interactions, and a sense of belonging are key benefits of living in these prime districts.

Key Features of the PLH Model

The PLH model introduces several features that distinguish it from standard HDB flats, ensuring both affordability and long-term community stability. These features impact eligibility, resale, and rental options, making it essential for buyers to understand them fully.

Extended Minimum Occupation Period (MOP)

One of the most significant features of the PLH model is the 10-year Minimum Occupation Period (MOP), compared to the standard 5 years for typical HDB flats. This is designed to curb speculative buying and encourage genuine homeownership in prime locations.

| Flat Type | MOP Duration | Purpose |

|---|---|---|

| Standard HDB | 5 years | Encourages homeownership |

| PLH Flats | 10 years | Reduces speculative buying; fosters community |

Key Points:

- Longer MOP promotes stable, long-term communities.

- Reduces speculative flipping and quick resale profits.

- Buyers should plan for a longer stay before upgrading.

Think of the 10-year MOP as a commitment to your neighbourhood. It’s perfect for those who value community over quick returns.

Additional Subsidies with Subsidy Recovery

PLH flats come with additional subsidies to make these homes more affordable for Singaporeans. However, to prevent windfall profits, a subsidy recovery applies when the flat is sold.

Key Points:

- Extra subsidies reduce upfront costs for buyers.

- Upon resale, owners repay a percentage of the resale price to HDB (subsidy recovery).

- This ensures the next buyer can still afford the flat at a fair price.

For insights into the latest home loan rates in Singapore, check out Ace Mortgage — they provide up-to-date advice to help you plan your finances.

Restrictions on Renting Out Entire Flats

Even after fulfilling the MOP, PLH flat owners cannot rent out their entire unit. This ensures that prime areas remain occupied by owners, not investors or transient tenants.

Key Points:

- Renting out individual rooms is allowed.

- Keeps prime areas vibrant and community-focused.

- Discourages speculative investment.

I do think that renting restrictions can feel limiting, but they truly preserve the social fabric of prime HDB neighbourhoods. It’s a small trade-off for a stable, community-rich environment.

For more on how the PLH model fits into your housing plans, explore our home loan comparison tools and latest blog posts.

Eligibility Criteria for PLH Flats

Understanding the eligibility criteria is crucial for prospective buyers considering a PLH flat in Singapore. The government has implemented strict guidelines to ensure these prime flats benefit genuine homeowners rather than investors.

Income and Citizenship Requirements

To keep PLH flats accessible to Singaporeans, eligibility is limited to Singaporean citizens with a household income not exceeding $14,000. This aligns with the income ceiling applied to standard Build-To-Order (BTO) flats.

| Criteria | Details |

|---|---|

| Citizenship | At least one applicant must be a Singapore Citizen |

| Household Income | ≤ $14,000 per month |

| Priority Group | First-timer families |

Key Points:

- Singaporeans are prioritised to build inclusive communities.

- Income ceiling ensures flats remain affordable.

- Priority given to first-timer families supports young couples.

Even if you’re close to the income ceiling, remember to factor in bonuses and additional income streams when calculating eligibility — exceeding the cap could disqualify your application.

Restrictions on Private Property Ownership

PLH applicants must not own or have disposed of any private property (local or overseas) within the past 30 months before application. This rule is designed to ensure that prime location flats go to those who genuinely need housing rather than to investors.

Key Points:

- No current or recent private property ownership.

- Includes local and overseas properties.

- Encourages fair access to prime housing.

For expert guidance on how private property ownership might affect your eligibility or loan rates, check out Ace Mortgage’s insights on refinancing and eligibility requirements.

Family Nucleus Requirement

Applicants must form a family nucleus to qualify — meaning singles are currently excluded from buying PLH flats. This rule helps support the government’s goal of fostering family-friendly communities in prime areas.

Key Points:

- Eligible family nucleus includes:

- Married couples.

- Engaged couples (with a marriage certificate within 3 months of key collection).

- Families with children.

- Widowed or divorced parents with children.

- Married couples.

- Singles are not eligible to apply for PLH flats.

While some may find the restrictions strict, they’re designed to foster vibrant communities where families can thrive. If you’re planning to buy in the future, keep your family plans in mind and start building eligibility early.

Explore more on HDB housing options in our latest blog posts — including tips on balancing family planning and homeownership.

Implications for Resale and Upgrading

The PLH model introduces resale and upgrading implications that every potential buyer should understand before making a purchase. While these flats offer prime locations at affordable prices, there are trade-offs that affect your long-term property goals.

Limited Pool of Eligible Resale Buyers

Unlike standard HDB flats, PLH flats have stricter eligibility criteria even in the resale market. Buyers must meet the same citizenship, family nucleus, and income requirements as original buyers.

| Eligibility Criteria | Details |

|---|---|

| Citizenship | At least one Singapore Citizen |

| Family Nucleus | Married couples or families only |

| Household Income Cap | ≤ $14,000 monthly income ceiling |

| Private Property Ownership | No property ownership in last 30 months |

Key Points:

- Resale pool is limited, which may affect demand.

- Potentially longer selling period due to eligibility checks.

- Sellers must manage expectations on resale prices.

If you’re thinking of buying a PLH flat with future resale in mind, plan for a longer selling period compared to standard flats. Factor this into your financial planning.

Impact on Upgrading Plans

The 10-year Minimum Occupation Period (MOP) and resale restrictions can delay your plans to upgrade to private property or larger homes. For homeowners with evolving family needs or aspirations to climb the property ladder, this is a key consideration.

Key Points:

- Upgrading plans may be postponed by at least 10 years.

- Planning a family or career change? Think ahead before committing.

- Longer MOPs give buyers stability but reduce flexibility.

For the latest home loan rates to support upgrading plans, check out Ace Mortgage’s comparison tools and expert refinancing guides.

Considerations for Investment Potential

While PLH flats are not designed for short-term gains, their prime locations can still offer long-term value appreciation. However, restrictions like the subsidy recovery and extended MOP dampen their investment potential compared to standard flats or private property.

Key Points:

- Long-term holding can still yield steady capital appreciation.

- Subsidy recovery reduces immediate resale profits.

- Not the best choice for speculative investors.

Think of a PLH flat as a lifestyle investment rather than a quick flip. If you’re looking for stable value in a prime location — and are willing to commit — PLH might still be the right fit.

For a deeper dive into investment potential and how it compares to other housing types, explore our latest blogs on refinancing and upgrading.

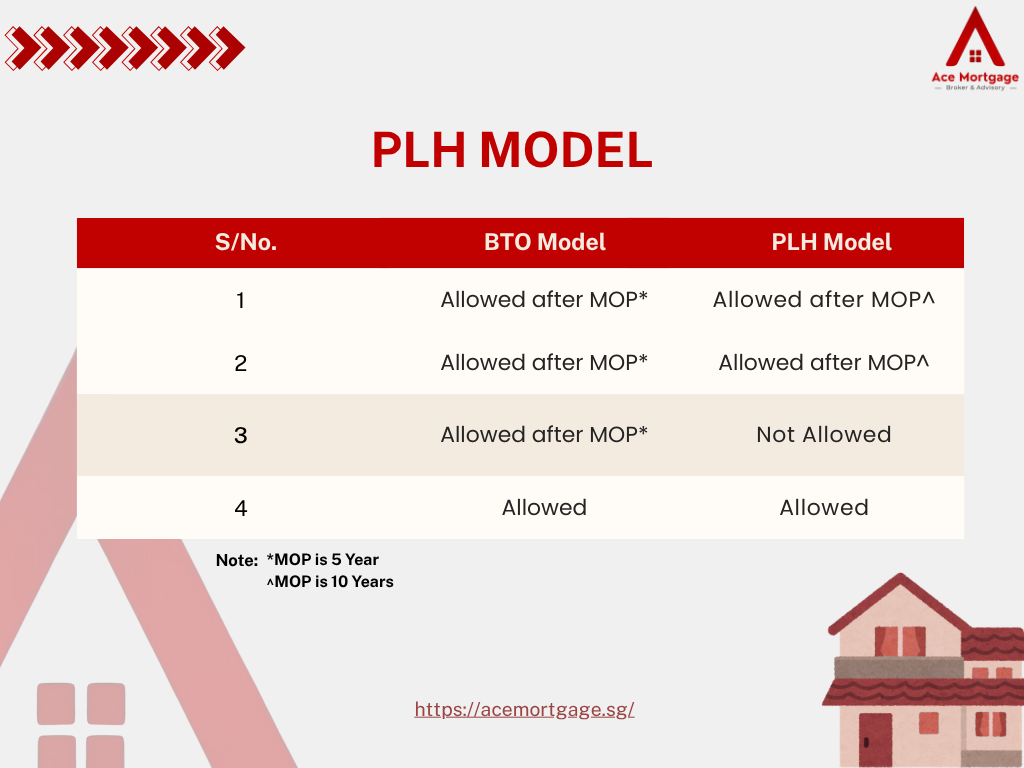

Comparing PLH with Other Housing Models

Understanding how the PLH model stacks up against other housing types — like Plus and Standard flats — is key to making the right choice for your family and financial goals.

Differences Between PLH, Plus, and Standard Flats

Each housing model in Singapore comes with its own set of restrictions, benefits, and resale considerations. Here’s how they compare:

| Feature | PLH | Plus | Standard |

|---|---|---|---|

| MOP | 10 years | 10 years | 5 years |

| Subsidy Recovery | Yes | Yes | No |

| Rental Restrictions | Cannot rent out entire unit | Cannot rent out entire unit | Can rent out entire unit |

| Location | Prime areas | City fringe areas | All other locations |

Key Points:

- PLH flats have the strictest resale and rental restrictions.

- Plus flats strike a balance with slightly more flexibility than PLH.

- Standard flats offer the most flexibility in rental and resale.

For a deeper look into how these models impact your homeownership plans, check out our comprehensive guide to refinancing and eligibility requirements.

Suitability for Different Buyer Profiles

Choosing the right housing model depends on your long-term goals, family situation, and lifestyle preferences.

Buyer Profiles to Consider:

- Young Families:

- PLH flats offer great locations near workplaces and amenities but come with longer MOPs and stricter eligibility.

- PLH flats offer great locations near workplaces and amenities but come with longer MOPs and stricter eligibility.

- Investors:

- Standard flats offer more flexibility for renting and resale.

- PLH is less ideal for short-term investment due to restrictions.

- Standard flats offer more flexibility for renting and resale.

- Retirees:

- Plus flats might provide a balance between location and fewer restrictions.

- Plus flats might provide a balance between location and fewer restrictions.

Think about how long you plan to stay in your flat and whether the restrictions align with your future plans. The longer MOP can work in your favour if you’re looking for stability and community.

Future Developments and Policy Adjustments

The property market is dynamic, and the government continually refines housing policies to keep public housing inclusive and fair.

What to Watch:

- Potential tweaks to eligibility criteria or subsidy structures.

- New locations released under the PLH model — keep an eye on upcoming BTO launches.

- Continuous monitoring of resale price trends and subsidy recovery to ensure affordability.

For the latest updates on home loan rates and expert analysis on future housing trends, visit Ace Mortgage.

It is good to stay informed and flexible — housing policies evolve to meet market demands and affordability goals. Planning ahead ensures you won’t be caught off-guard by changes.

Pros and Cons of the PLH Model

Every housing model has its benefits and limitations, and the PLH model is no different. Let’s break down the pros and cons so you can decide if it’s the right fit for you.

Advantages for Homebuyers

PLH flats offer several compelling benefits, especially for those who value location and community.

Key Advantages:

- Prime Locations: Close proximity to MRT stations, workplaces, and amenities.

- Affordability: Additional subsidies make prime housing more accessible to Singaporeans.

- Community Focus: Rental restrictions and longer MOPs foster stable, vibrant communities.

Buying a PLH flat means being part of a carefully planned community where neighbours are invested in the same long-term lifestyle — a big plus if you’re looking for stability and community spirit.

Potential Drawbacks to Consider

While the PLH model offers many perks, there are some limitations to keep in mind.

Potential Drawbacks:

- Longer MOP: The 10-year occupancy requirement may limit your flexibility.

- Rental Restrictions: You can’t rent out the entire flat, which reduces investment opportunities.

- Subsidy Recovery: You’ll need to pay back a portion of the subsidies if you sell, reducing resale profits.

For those planning to refinance after the MOP, Ace Mortgage offers guidance on how to navigate these restrictions and make the most of your home’s value.

Weighing the Trade-offs

Before deciding on a PLH flat, think carefully about your long-term plans and priorities.

Questions to Ask Yourself:

- Am I comfortable committing to a 10-year stay?

- Does the prime location outweigh the resale and rental limitations?

- How will subsidy recovery affect my future selling price?

I think that if you prioritise community, stability, and a convenient location, the PLH model might be a perfect fit. If you’re looking for quick gains or rental income, consider other housing models with fewer restrictions.

For more insights on balancing property investment and lifestyle, check out our latest mortgage guides and comparison tools.

Conclusion: Is the PLH Model Right for You?

Choosing a home is one of the biggest decisions you’ll make — and the PLH model comes with unique benefits and trade-offs. Here’s how to decide if it’s the right fit for your housing journey in Singapore.

Assessing Your Housing Priorities

Start by clarifying what matters most to you in a home.

Ask Yourself:

- Do I value living in a prime location with convenient access to work, schools, and amenities?

- Am I comfortable with a longer Minimum Occupation Period (MOP) of 10 years?

- Will the community-building aspect of PLH enhance my living experience?

If lifestyle and community matter more than short-term resale gains, a PLH flat could be the right choice for your family.

Navigating the Application Process

Applying for a PLH flat requires meeting strict eligibility criteria, so it’s essential to plan ahead.

Key Steps:

- Review the eligibility requirements — including income, citizenship, and private property ownership.

- Gather your documents early to avoid delays.

- Check the latest BTO launches and ballot wisely — competition is high.

For an easy way to estimate home loan repayments, use the Ace Mortgage calculator to plan your finances effectively.

Planning for the Future

The PLH model is designed for long-term living, so plan accordingly.

Consider:

- Future family plans and space needs — think beyond today’s requirements.

- How restrictions might affect upgrading or investing in the property market later on.

- Staying updated on policy changes that could affect your resale or refinancing plans.

Ready to take the next step towards your dream home? Whether you’re exploring the PLH model or comparing other housing options, our team at Ace Mortgage is here to guide you.

Reach out today to get the latest home loan rates, personalized advice, and step-by-step support on your property journey. Your dream home in Singapore’s prime location is just a click away.