Planning to buy a home? Whether it’s a resale HDB or a shiny new condo, there’s one crucial step you don’t want to overlook — the bank valuation.

It’s not just a formality. A low bank valuation can shrink your loan amount, increase your cash top-up, or even derail your mortgage application.

In this quick guide, we’ll explain how bank valuation for mortgage in Singapore works, why it matters, and what to watch out for before applying.

What Is a Bank Valuation and Why Does It Matter?

If you’re applying for a home loan in Singapore this year, here’s something you need to know upfront: what you agree to pay for a property isn’t always what the bank thinks it’s worth.

And when it comes to getting your mortgage approved, the bank’s opinion is the one that counts.

How is bank valuation different from market or agent valuation?

Let’s break it down:

- Market valuation = what buyers are willing to pay

- Agent valuation = often influenced by asking prices

- Bank valuation = based strictly on data and risk models

Banks don’t factor in renovated kitchens or sea views. They look at recent sales, location data, and internal formulas to decide how much the property is safely worth — for loan purposes.

For example:

A seller might list a condo at $1 million, but if the bank values it at $950,000, that’s the number your mortgage is based on — not the seller’s price.

Expert tip: Always check the bank valuation before signing the OTP. It’s free to check, and could save you from a painful cash shortfall later.

Why do banks use conservative valuations for mortgage approval?

Banks are risk-averse. Their goal is to avoid lending more than a property can realistically fetch in the resale market — especially in a downturn.

That’s why bank valuations in Singapore tend to be on the conservative side. With the property market cooling and interest rates still fluctuating, lenders are extra cautious.

They’re especially strict when:

- The property is in a new launch with little transaction history

- The seller is asking well above recent sales

- The unit has unusual features (e.g. odd layout, top floor premium)

Real-world insight: Many buyers assume the bank will match their offer price. That’s rarely the case — especially for resale condos or under-valued HDBs in hot areas.

What role does it play in determining your home loan amount?

Here’s the key part: your loan-to-value (LTV) ratio is based on the lower of:

- The purchase price

- The bank’s valuation

Let’s say:

- Purchase price = $1,000,000

- Bank valuation = $950,000

→ Your max loan = 75% of $950,000 = $712,500

You’ll need to fork out the $287,500 difference through cash or CPF. And that’s before stamp duty or legal fees.

Bottom line: Even if you qualify for a large mortgage loan in Singapore, the bank valuation decides how much you actually get. That’s why smart buyers get this sorted first — or work with a mortgage broker in Singapore who can check valuations across banks before you commit.

How Do Banks Determine the Valuation of Your Property?

If you’re applying for a mortgage loan in Singapore, it’s not just about what you’re willing to pay — it’s about what the bank thinks the property is worth.

And that number? It comes from a surprisingly calculated process that’s often more conservative than buyers expect.

What criteria do banks use — price history, comparables, facing?

Banks don’t guess. They assess your property based on recent sales data, the unit’s characteristics, and the surrounding market. Here’s what typically goes into a bank valuation for mortgage approval in Singapore:

Key Factors Banks Use to Calculate Property Valuation in Singapore

| Valuation Factor | What It Means |

|---|---|

| Recent transactions | Prices of nearby units sold within the last 6–12 months |

| Unit size and floor level | Larger and higher-floor units may fetch better valuations |

| Facing and layout | Direction, privacy, and efficiency of layout can impact value |

| Development reputation | Respected developers and well-managed condos score better |

| Location & amenities | Proximity to MRTs, schools, parks, and malls adds valuation weight |

| Age and condition | Older units or poorly maintained ones may be valued lower |

Expert tip: Agent quotes often don’t align with what banks will lend. Always check with your mortgage advisor before committing to an Option to Purchase (OTP).

What is an AVM (Automated Valuation Model) and how accurate is it?

Most banks today use AVMs — automated valuation models — to get a quick estimate without needing an on-site visit.

These tools rely on:

- HDB and URA resale data

- Transaction volume in the project/area

- Internal bank risk scoring models

They’re fast, low-cost, and accurate most of the time — especially for standard HDB flats and mass-market condos.

But they’re not perfect. AVMs may undervalue properties that are rare, renovated, or have unique layouts.

When do banks conduct physical or desktop inspections?

Not all valuations are done with AI. Some still require human judgment — especially when:

- No recent transactions exist for the unit type

- It’s a landed property or boutique development

- The AVM shows outlier results

- The borrower requests a review due to renovation or appeal

Here’s how it typically breaks down:

Comparison of Bank Valuation Methods Used for Mortgage Approval in Singapore:

| Valuation Method | When It’s Used |

|---|---|

| AVM (Automated) | Default for HDBs, condos with recent transactions |

| Desktop valuation | Used for special cases, with floorplans and visual data |

| Physical inspection | Landed homes, unique units, or when the buyer challenges the AVM |

Personal tip: If you’re buying a rare unit (e.g. high-floor corner or renovated resale flat), a physical inspection might help push the valuation up — which means borrowing more and topping up less.

What Happens If the Valuation Differs from the Purchase Price?

So you’ve found your dream home, negotiated a price, and applied for your loan — but the bank comes back with a lower valuation than what you offered. Now what?

This scenario is more common than most buyers realise in Singapore, especially for resale condos, new launches with hype pricing, or unique HDB flats. And yes, a low bank valuation can seriously affect your mortgage loan and upfront cash requirement.

What should you do if your bank valuation is lower than expected?

First, don’t panic — but don’t ignore it either.

If the bank valuation comes in lower than the agreed purchase price, it doesn’t mean your deal is dead. But it does mean you’ll have to cover the shortfall — typically in cash (not CPF), since banks will only lend based on the lower of the two values.

Example:

- Purchase price: $1,000,000

- Bank valuation: $950,000

→ Shortfall = $50,000 (cash top-up required)

Expert tip: Before you sign the OTP, work with a mortgage broker in Singapore to check valuation ranges from multiple banks — some may offer a higher valuation than others for the same unit.

How does it affect LTV, downpayment, and CPF usage?

The Loan-to-Value (LTV) ratio in Singapore is capped at 75% for bank loans. But here’s the catch — it’s 75% of the bank’s valuation, not the price you agreed to pay.

Here’s how a low valuation shifts your numbers:

Impact of Low Bank Valuation on Home Loan Amount and Downpayment

| Scenario | High Valuation | Low Valuation |

|---|---|---|

| Purchase Price | $1,000,000 | $1,000,000 |

| Bank Valuation | $1,000,000 | $950,000 |

| Max Loan (75% of valuation) | $750,000 | $712,500 |

| Buyer’s Cash/CPF Needed | $250,000 | $287,500 + $50K cash top-up |

This means you’ll need to fork out more upfront if the valuation is low — and that extra top-up must usually be in cash.

Tip: If you’re tight on funds, consider appealing the valuation or negotiating with the seller — especially if your bank valuation is significantly below market.

Can you get a second opinion or appeal for a revaluation?

Yes — and you should, especially if:

- You believe the valuation missed out on key comparables

- The property was recently renovated or upgraded

- Another bank values it higher

Most banks allow you to request a revaluation or submit your own valuation report from an approved valuer. Alternatively, a different bank may use a different AVM model and provide a higher figure — which could get you a better loan deal.

Pro tip: If your valuation is low, don’t rush to sign. Compare across banks and use the one that gives you the best combination of valuation + interest rate — not just the cheapest headline rate.

What Does a Bank Valuation Report Include?

A bank valuation report might not be something most buyers ever see — but it’s central to your home loan approval. This document determines how much the bank believes your property is worth and, in turn, how much they’re willing to lend you.

Understanding what’s in this report can help you avoid surprises — and even challenge an undervaluation if needed.

Who prepares the report and how long does it take?

Bank valuation reports are typically prepared by:

- In-house valuation teams (for major banks like DBS, UOB, OCBC)

- Or by external professional valuers from firms like Knight Frank, Edmund Tie & Co, or Savills — depending on the bank’s policy

The process depends on the type of valuation:

- Automated (AVM): Instantly generated — often same day

- Desktop valuation: ~1–3 working days

- Full inspection: ~3–5 working days depending on access and scheduling

Expert tip: If you’re racing against an OTP deadline, request the valuation as early as possible — delays can bottleneck the entire mortgage loan application process.

What key details are listed in the bank’s valuation report?

The report may be brief or detailed depending on the bank and property type, but it typically includes:

Key Information Found in a Property Valuation Report in Singapore

| Valuation Report Section | What It Covers |

|---|---|

| Property description | Type (HDB, condo, landed), address, size, tenure |

| Market value (SGD) | The final assessed value used for loan calculations |

| Valuation date | Date the valuation was performed |

| Method used | AVM, desktop, or physical inspection |

| Comparables | Reference to similar recent transactions (price, unit, distance) |

| Assumptions/limitations | Notes on condition, market volatility, or info gaps |

Note: For landed homes, reports are usually more detailed. For HDBs and standard condos, the report might just contain the value and methodology used.

Can you request a copy, and will it differ between banks?

You can request a copy — but whether you receive it depends on the bank. Some provide it upon request, especially for private property loans. Others may only communicate the final valuation figure without releasing the full report.

Yes, valuation results can differ across banks, because:

- Each bank may engage different valuation firms

- AVMs are built on proprietary data models

- Valuation assumptions may vary (e.g. weighting of renovations or rare layouts)

Pro tip: If your bank valuation in Singapore feels off, ask a mortgage broker to check with other lenders. Some banks may give you a higher figure — which could save you tens of thousands in cash top-up.

How Much Does a Property Valuation Cost in Singapore?

If you’re applying for a home loan in Singapore, don’t forget to factor in the valuation fee. While it’s not the biggest cost in the process, it’s essential — and in some cases, avoidable depending on how you work with your bank or broker.

Here’s what you should expect in terms of valuation costs for HDB flats, private condos, and landed properties.

What are typical fees for HDB, condos, and landed homes?

Valuation fees vary based on property type, size, and whether a physical inspection is needed.

Average Property Valuation Fees in Singapore (2025)

| Property Type | Valuation Method | Estimated Fee (SGD) |

|---|---|---|

| HDB Flat | AVM / Desktop | Usually free if done via HDB portal or selected banks |

| Condo (Standard) | Desktop / Physical | ~$150 to $350 |

| Condo (Premium/Unique) | Physical inspection | ~$350 to $500+ |

| Landed Property | Always physical | $500 to $800+ |

Expert tip: Some banks may waive the valuation fee if you take up their home loan package. Always ask upfront or check to see who’s offering this perk.

When do you pay the valuation fee — and is it refundable?

Here’s how it works:

- If you’re buying an HDB resale flat, you usually request valuation through the HDB portal after getting the Option to Purchase (OTP). There’s no fee.

- For bank valuations on condos or landed homes, the fee is typically charged before or during loan application.

- If your loan falls through or you switch banks later, the fee is usually non-refundable.

Personal tip: If you’re comparing banks, don’t request multiple valuations upfront — lock in your preferred lender first to avoid paying twice.

How long is a valuation report valid for?

Valuation reports aren’t forever. Banks usually treat valuations as valid for:

- HDBs & Condos: 3 months

- Landed Properties: 1 to 2 months, depending on market conditions

After that, the bank may:

- Require a revalidation (small admin fee or updated report)

- Or request a new valuation entirely, especially in a volatile market

Tip: Plan your purchase timeline carefully. If your valuation expires before loan disbursement, it can cause unnecessary delays or even require you to top up more cash if prices have changed.

How Do Valuations Work for New Launch or BUC Properties?

Buying a new launch unit? You’re not just paying for a home — you’re buying future value. Since these properties are still under construction, banks need to assess risk differently when determining how much they’re willing to loan.

And yes, BUC valuations can vary between banks — and change over time.

How is valuation done when the property is still under construction?

Unlike resale units, BUC properties don’t have recent transactions, physical inspections, or full furnishings to work with. So banks rely heavily on:

- Developer launch price

- Floor level and facing

- Unit type and stack

- Pricing of comparable past launches nearby

- Internal AVM (Automated Valuation Model) estimates

- Confidence in the developer and project profile

Since there’s no physical unit to inspect, BUC valuations are desk-based — but still critical. The bank needs to decide what the completed unit will be worth by the time it’s ready.

Always check the bank valuation before booking a BUC unit, especially if you’re stretching your budget. Even if the launch price is developer-approved, some banks may still value it lower than expected.

Do different banks give different values for the same BUC unit?

Yes — and this happens more often with new launches than resale.

Different banks have:

- Different valuation databases and internal models

- Varying confidence levels in specific developers or locations

- Unique risk tolerance for future market conditions

So while one bank may accept your BUC purchase price at face value, another may value it $20K–$40K lower, requiring a cash top-up to bridge the gap.

What happens if the valuation drops before the TOP date?

This is where many BUC buyers get caught off guard.

If the property market cools between your booking date and the Temporary Occupation Permit (TOP) date, banks may revalue the property lower when it’s time to disburse the loan.

Here’s what can happen:

- The bank reduces the loan quantum

- You’re asked to top up more cash or CPF

- Your LTV may be recalculated based on the lower valuation

- In worst cases, financing may fall short altogether

My word of advice is that If your BUC unit’s TOP is still years away, build in a buffer. Property valuations can drop — and if they do, you’ll be responsible for making up the difference, not the bank.

Common Real-World Valuation Scenarios (With Examples)

Bank valuations in Singapore don’t always match the price you agree to — and the fallout can be expensive. Here are real examples of how valuation gaps have impacted buyers, and how to protect yourself.

Case study: HDB valuation lower than resale price — what happened?

The situation:

A couple was ready to buy a 4-room resale HDB in Bishan for $720,000. But the bank valuation came back at $680,000, forcing them to top up $40,000 in cash (not CPF).

Why it happened:

- Overpriced due to renovations

- Lack of recent high-floor resale data

- Bank’s AVM model used conservative comparables

Tip: Always check the valuation first. If you’re buying an HDB flat, start with our HDB home loan guide to understand loan limits and how valuation affects your CPF usage.

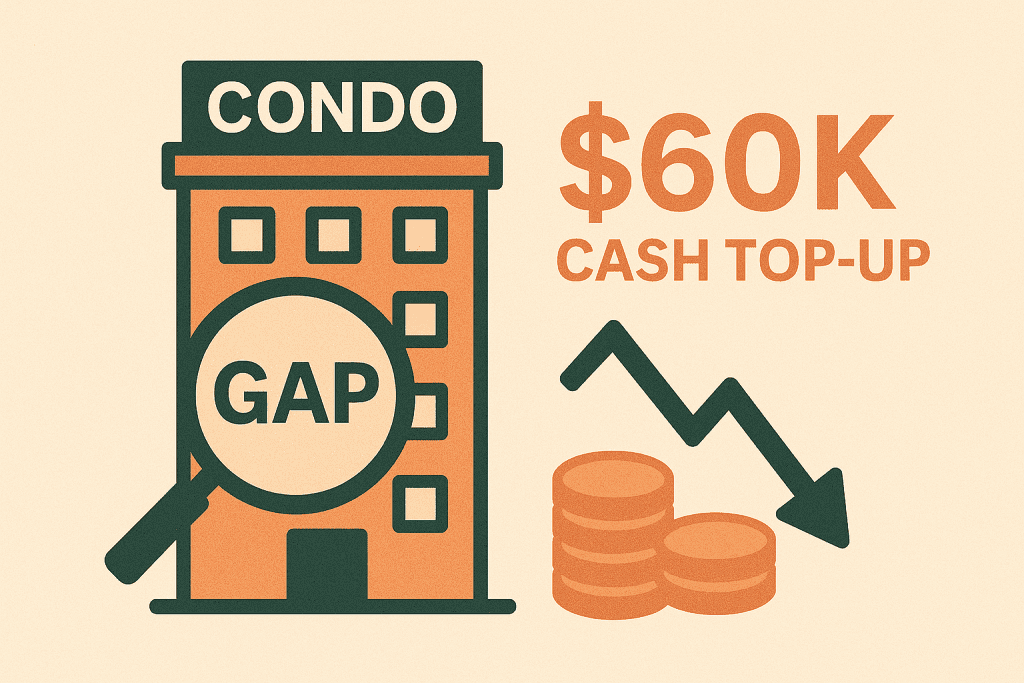

Example: Condo valuation gap and the need for $60K cash top-up

The situation:

A buyer booked a new condo unit for $1.5M, only to find that the bank valuation was just $1.42M. The result?

- Loan was capped at $1.065M

- Buyer had to fork out an extra $60K in cash

Why it happened:

- New launch pricing stretched beyond surrounding market norms

- Bank had fewer comparables for that stack/facing

- AVM returned a cautious estimate

Expert insight: If you’re buying private property, make sure to compare both bank valuations and home loan rates in Singapore. Our private property loan guide explains how banks assess condos and landed homes — and what to do if valuations fall short.

When it’s better to switch banks for a better valuation outcome

The situation:

A couple buying a resale EC got a valuation of $1.02M from one bank. But their mortgage broker found another lender who valued the same unit at $1.08M.

The impact?

- Higher loan eligibility

- Avoided a hefty cash shortfall

- Secured a better interest rate package

Pro tip: Not all banks use the same models. Some may offer better condo loan packages or more flexible home loan interest rates in Singapore. Compare multiple banks at once using our condo loan guide or speak with a mortgage expert for faster results.

Bank Valuation Trends & Policy Updates

Bank valuations in Singapore aren’t static — they evolve based on policy shifts, technology trends, and market conditions. We’re seeing clear changes in how banks approach valuation, especially in response to tighter lending rules and smarter data tools.

If you’re applying for a home loan in Singapore this year, here’s what you need to know.

How cooling measures affect valuation methodology

With the latest property cooling measures still in effect, banks have become noticeably more conservative in their valuations. This is especially true for:

- HDB resale flats with Cash Over Valuation (COV)

- New launch condos in fringe districts

- High-end units with unverified premiums

Why? Because the Loan-to-Value (LTV) limits, Total Debt Servicing Ratio (TDSR), and Additional Buyer’s Stamp Duty (ABSD) all reduce affordability — and banks are pricing risk accordingly.

Expert tip: If you’re unsure how recent policies affect your financing, start with our mortgage interest rate guide or check specific bank packages like DBS home loans or UOB home loans to compare current risk premiums.

Are banks relying more on AVMs or AI-generated data today?

Banks are doubling down on Automated Valuation Models (AVMs) and integrating AI-based predictive tools. These tools draw on:

- URA and HDB resale databases

- AI-driven market forecasts

- Internal risk engines that factor in buyer profile and loan history

While this means faster turnaround times for valuation reports, it also means less human discretion — so unique units (e.g. penthouses, corner stacks, heavily renovated homes) may be under-valued.

Our view: If you’re buying a non-standard unit, don’t rely on AVM alone. Engage a mortgage advisor who can request desktop or physical valuations if needed.

What you need to know about MAS, IRAS, and URA rule updates

Three authorities influence valuation directly or indirectly:

- MAS (Monetary Authority of Singapore)

- Oversees LTV, TDSR limits

- Stricter enforcement of income-based loan ceilings

- Emphasises prudence in high-interest environments

- Oversees LTV, TDSR limits

- IRAS (Inland Revenue Authority of Singapore)

- Buyer’s Stamp Duty (BSD) and ABSD rates have a knock-on effect on loan sizes

- Refer to our BSD calculator to check your upfront costs

- Buyer’s Stamp Duty (BSD) and ABSD rates have a knock-on effect on loan sizes

- URA (Urban Redevelopment Authority)

- Provides land sales data and zoning information used in bank AVMs

- Updates in zoning (e.g. leasehold restrictions, plot ratio changes) can shift valuation projections

- Provides land sales data and zoning information used in bank AVMs

Note: All three bodies influence how much banks are willing to lend — even if it’s not immediately obvious. Always check updated policies or use our mortgage calculator to reassess affordability before signing your Option to Purchase.

How to Prepare for a Stronger Bank Valuation

While you can’t control the market, you can influence how your property is perceived during the bank valuation process. Especially where valuations can vary across banks and even small gaps can cost you thousands — it’s smart to take a few steps to boost your chances.

Here’s how to get the most out of your valuation.

What documents and details help support your property’s value?

The more accurate and complete the info, the better. Here’s what to prepare before your valuation (especially for desktop or physical inspections):

- Floor plan with correct square footage

- Proof of recent renovations (invoices, before/after photos)

- Comparable transactions in the same development

- Official records showing leasehold duration or upgrades

- MCST maintenance records (for condos)

Pro tip: If you’re working with a mortgage broker in Singapore, they can help prep this pack and even liaise with the bank’s valuer directly.

Does interior renovation affect the final bank valuation?

Yes — but not as much as most people think.

Banks do factor in renovation quality, but they don’t value it dollar-for-dollar. A $100K renovation might only add $10K–$30K to your valuation, depending on:

- Market norm in the area

- Type of upgrades (functional vs aesthetic)

- Long-term durability of finishes

- Whether the upgrades boost rental or resale value

If you’ve recently renovated your condo or HDB flat, share the receipts and photos during the valuation process. It may help justify a higher value — and that means better loan-to-value (LTV) and potentially less cash top-up.

Should you time your valuation request based on market movement?

Absolutely — timing matters more than most buyers realise.

Banks base their valuation largely on recent transactions (usually past 3–6 months). So if:

- Nearby units have sold at higher prices recently = higher AVM score

- Market is cooling = conservative estimates expected

- The project is gaining traction (e.g. near TOP or MRT upgrade) = better value

Our view: If you’re purchasing a BUC or resale condo, ask your advisor whether it’s better to lock in the valuation now or later. Use our mortgage calculator to simulate different LTV scenarios before committing.

Frequently Asked Questions

Still unsure about how bank valuations work? Here are some of the most common questions buyers and homeowners in Singapore ask when navigating the property loan process.

Can I use the same valuation for refinancing or another bank?

Not usually. Each bank typically requires its own valuation report, especially if you’re switching lenders during a home loan refinance in Singapore.

- For refinancing, your new bank will want to verify the current market value themselves — using their own internal team or approved valuers.

- Valuation fees may apply again, unless the bank offers a free valuation as part of a refinancing promotion.

Tip: If you’re considering a switch, check out our full guide on refinancing your home loan — or for public flats, refinancing your HDB loan.

How many times can I request a valuation for the same property?

There’s no hard limit — but banks don’t appreciate repeated requests unless there’s a valid reason, such as:

- A significant change in recent transactions

- A new renovation that boosts value

- A different unit type becoming available for comparison

Keep in mind:

- Too many requests may lead to slower processing or extra admin fees

- If you’re shopping around for the best valuation, it’s more efficient to do it through a mortgage broker who can check multiple banks in parallel

What if my agent says the property is worth more than the bank says?

It’s very common for agents (and sellers) to quote higher prices than what banks will actually finance.

- Your agent may be basing their estimate on asking prices or emotional premiums (e.g. renovations, view, rarity)

- Banks, however, base their valuation on transaction history and internal risk models

Reminder: The bank’s number is what matters when it comes to financing. If there’s a shortfall, you’ll need to top up the difference in cash — even if you feel the price is justified.

Before making any decisions, use our mortgage loan calculator to understand how valuation affects your loan amount and monthly repayments.

Final Thoughts: Always Check the Valuation Before You Commit

Whether you’re buying your first flat, upgrading to a condo, or refinancing your mortgage — one thing remains the same: bank valuation can make or break your home loan.

It doesn’t matter what the seller or agent says your property is worth — the only number that determines your loan-to-value (LTV), downpayment, and cash outlay is what your bank believes it’s worth.

Smart move: Always check the valuation early — before you sign the OTP, before you choose a bank, and definitely before you commit to any big cash outlay.

If you’re unsure where to start, let us help. At Ace Mortgage, our advisors can compare valuations across multiple banks and help you find the best home loan rates in Singapore — with fewer surprises and better peace of mind.

Explore your options now: